- The paper introduces a fully implementable tamed Euler scheme to reliably approximate Lévy-driven SDEs with superlinear drift and diffusion.

- It establishes explicit strong Lp convergence rates, quantifying error contributions from discretization, jump truncation, and Monte Carlo estimation.

- Empirical experiments confirm theoretical convergence and stability, highlighting applicability in quantitative finance and stochastic simulations.

Strong Convergence and Regularity of Tamed Euler Approximations for Lévy-driven SDEs

This work addresses the numerical approximation of stochastic differential equations (SDEs) driven by Lévy processes, especially in the presence of superlinear drift and diffusion coefficients. Lévy-driven SDEs arise frequently in quantitative finance and various applied fields where discontinuous, event-driven stochasticity is fundamental. The standard Euler-Maruyama scheme is known to fail in this context due to the divergence in moments when coefficients grow faster than linearly. This paper proposes a fully implementable tamed Euler-type scheme, specifically engineered for Lévy-driven SDEs, to address these limitations. The main contributions include strong Lp convergence and temporal-spatial regularity results for the proposed method, together with explicit dependence of the scheme on initial conditions and time, and a comprehensive set of numerical experiments supporting the theoretical findings.

The general SDE under consideration is

dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)

where Wt is a Brownian motion, π~ is the compensated Poisson random measure associated to the Lévy process, and μ,σ,γ may exhibit superlinear growth. Diffusion and jump coefficients may not satisfy global Lipschitz conditions, creating both theoretical and computational challenges.

Tamed Euler Scheme Construction

The tamed Euler scheme is designed to overcome the divergence of explicit methods for superlinearly growing coefficients. The central idea is to "tame" each coefficient, rescaling its magnitude at each step according to both the step size and the norm of the current state. Specifically, for small step size δ and taming exponent χ≥1, the coefficients in the Euler step are replaced by

μδ(x)=(1+δ1/2∥x∥χ)1/2μ(x),σδ(x)=(1+δ1/2∥x∥χ)1/2σ(x)

and the jump integral is simulated with truncation of small jumps and Monte Carlo estimation for the jump compensator.

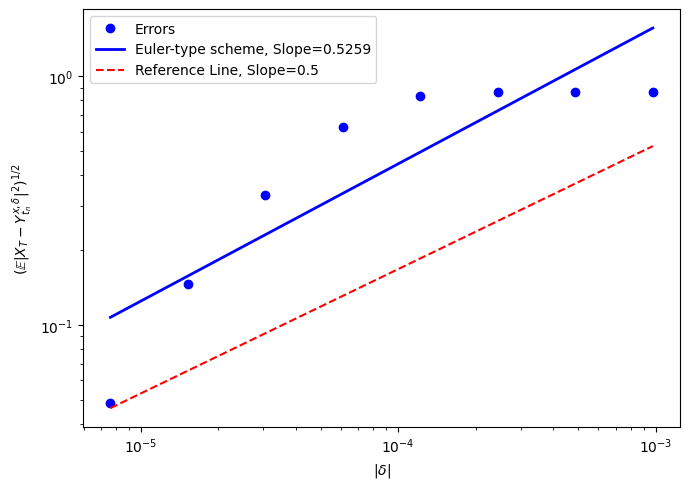

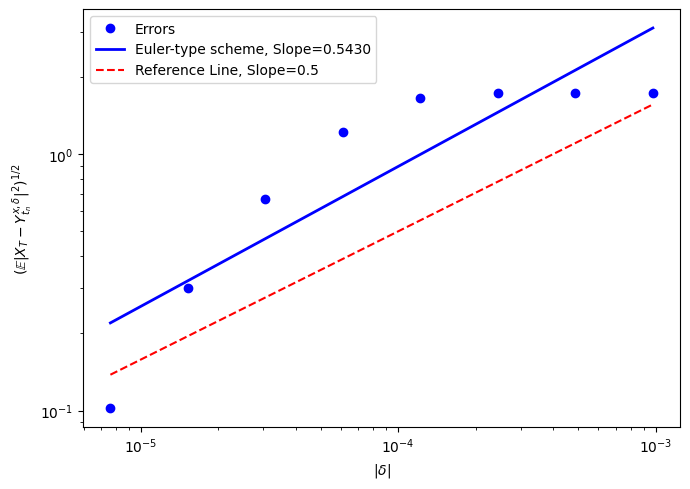

Figure 1: Simulation results for the tamed Euler scheme for a polynomial-growth SDE driven by a Lévy process, illustrating the empirical convergence rate in L2.

The full implementability of the method is achieved by (1) truncating small jumps (which renders the Lévy measure finite), and (2) employing a Monte Carlo average to approximate the jump compensator. The construction is fully specified and provably stable for a large class of Lévy-driven SDEs with superlinear coefficients, under conditions that generalize one-sided Lipschitz and polynomial Lipschitz properties to non-globally Lipschitz settings.

Main Results: Strong Convergence and Regularity

Strong Convergence

The central theorem quantifies the Lp approximation error of the tamed Euler scheme dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)0 relative to the true solution dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)1:

dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)2

where dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)3 is a polynomial in dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)4, dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)5 is the jump truncation threshold, dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)6 is the Monte Carlo sample size, and dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)7 is arbitrary (the convergence rate is thus arbitrarily close to dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)8). The three error contributions—discretization, jump truncation, and Monte Carlo estimation—are explicit.

The empirically observed dXt=μ(Xt−)dt+σ(Xt−)dWt+∫Rdγ(Xt−,z)π~(dz,dt)9 rate is close to Wt0 even for non-Lipschitz SDEs, aligning with the theoretical bound.

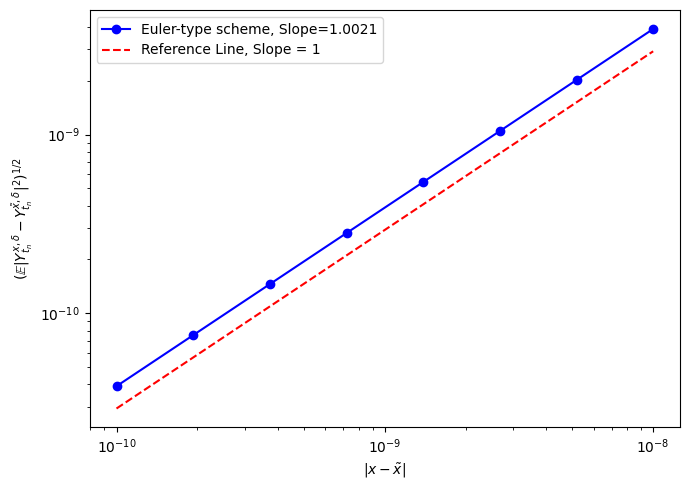

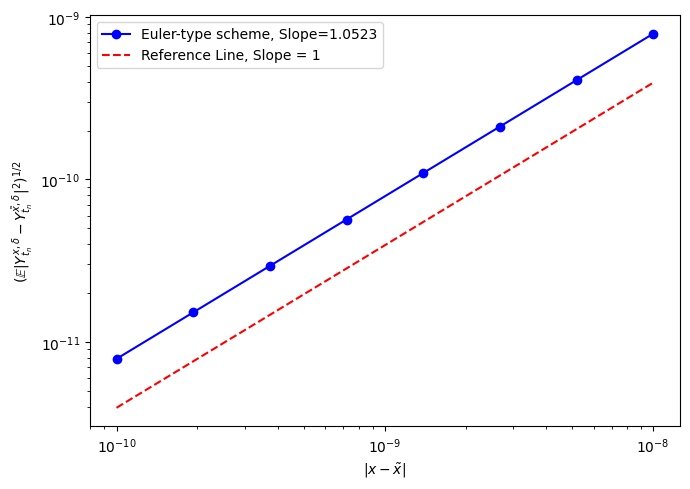

Figure 2: Numerical results for a Lévy-driven 3/2-volatility SDE, again showing Wt1 errors that match the theoretically predicted rates for the tamed Euler method.

Temporal-Spatial Regularity and Stability

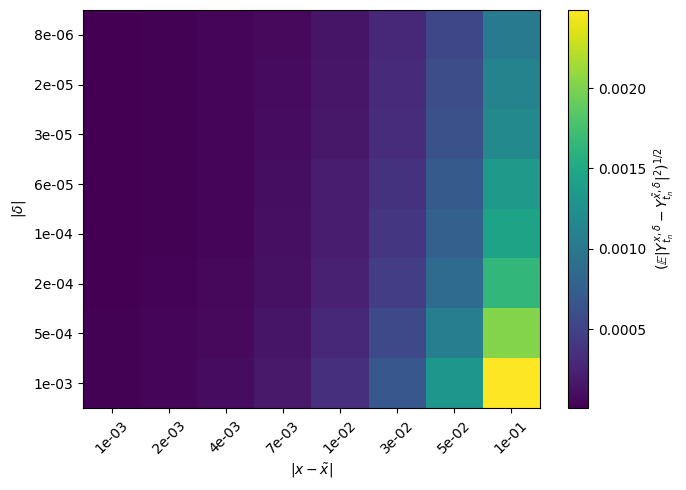

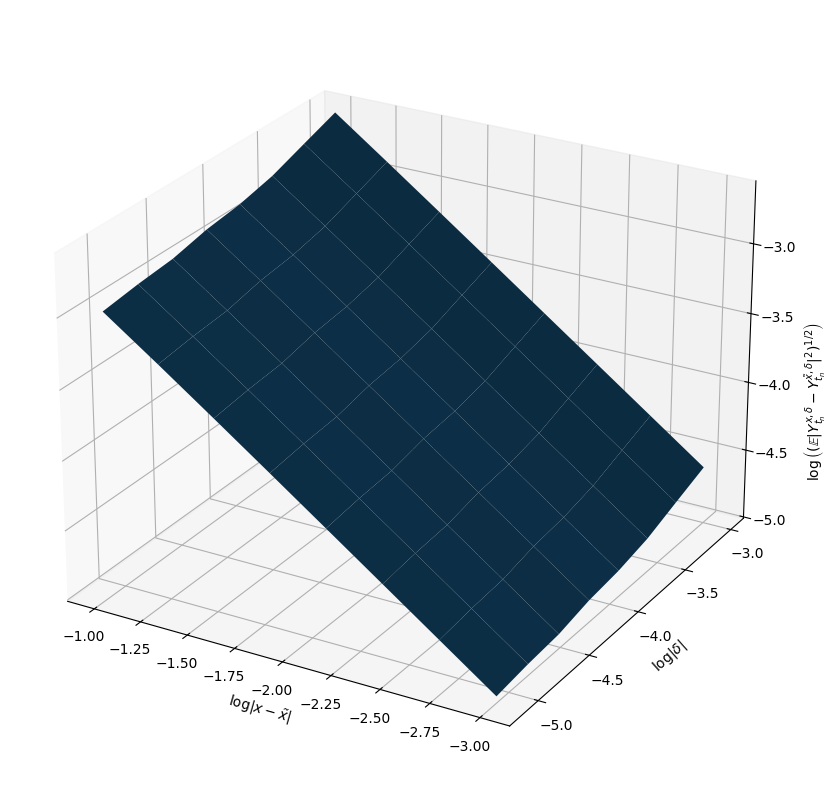

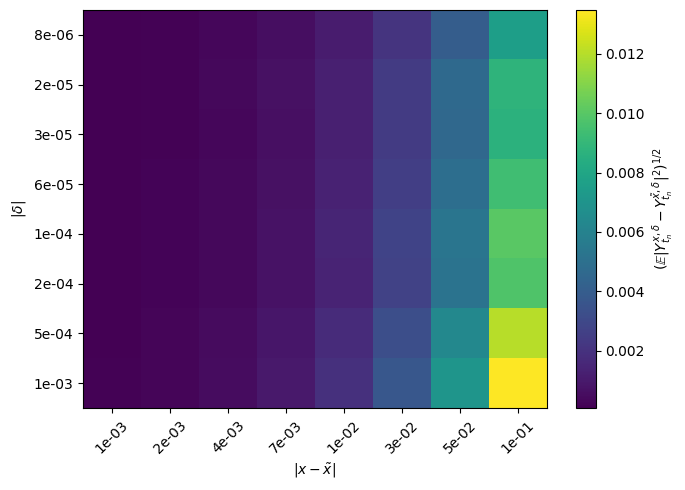

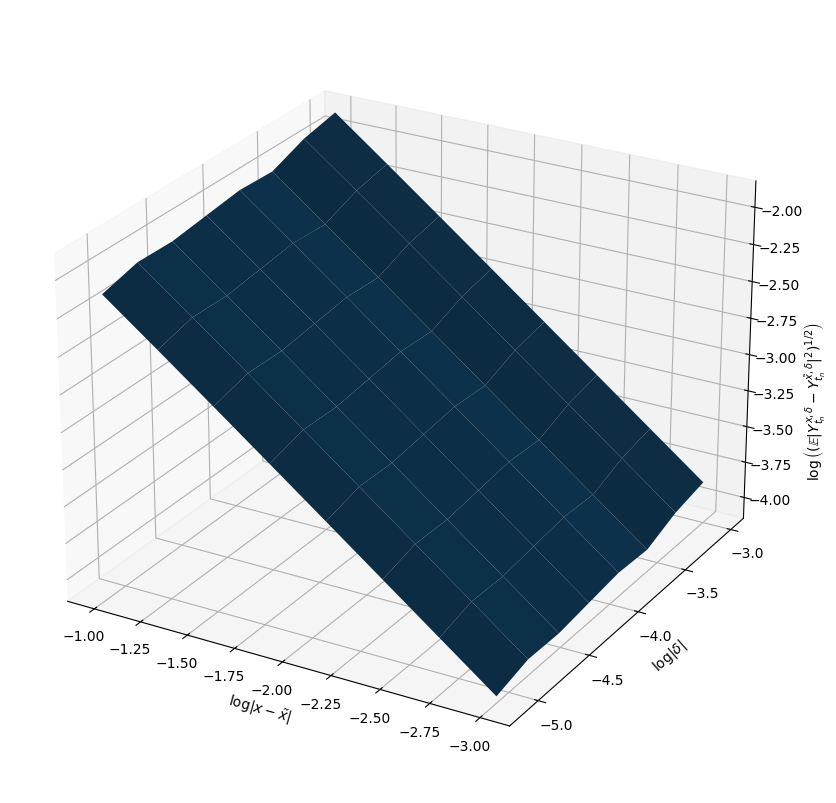

The paper provides quantitative continuity estimates with respect to initial state, initial time, and evaluation time. For any Wt2 and Wt3,

Wt4

where Wt5 is again polynomial in the initial norm, and the constants depend explicitly on step size and truncation. As step size vanishes, continuity in all variables is recovered. These properties are essential for the analysis and application of multilevel and multigrid Monte Carlo methods, as well as for proofs of correctness of algorithms for PDEs with Lévy noise.

Numerical Experiments

Two detailed numerical experiments are provided:

- Polynomial-Growth SDE: A standard cubic drift with quadratic diffusion and linear jump size, driven by a compound Poisson process with Gaussian jump sizes. The taming is observed to be crucial for the stability and convergence of the method. Strong convergence (with rate close to Wt6), linear dependence on initial value perturbations, and correct regularity in joint time-step / spatial perturbations are empirically demonstrated.

- Lévy-driven 3/2-type Volatility Model: This model is challenging due to the high nonlinearity (Wt7) and relevance in financial math. The proposed scheme is stable and accurate under realistic intensities and jump distributions, matching both theoretical rates and confirming robustness with respect to both time-step and initial data.

Theoretical and Practical Implications

From the theoretical perspective, the results extend the established convergence theory for Euler-type methods to SDEs with non-globally Lipschitz drifts, polynomial nonlinearity, and Lévy jumps. This closes an important gap in the theory, as prior results were confined to globally Lipschitz or purely Brownian-motion-driven cases.

On the practical side, these advances justify the use of tamed explicit schemes in computational finance and applied stochastic analysis, including Monte Carlo algorithms for nonlinear PDEs with jump terms via multilevel and multigrid discretizations. The explicit error decomposition guides the selection of parameters (step size, jump truncation, sample size) to balance computational efficiency and required accuracy.

This work also motivates further research in several directions:

- Adaptive taming factors for higher-order and multidimensional SDEs with Lévy noise.

- Rigorous extension of the method to infinite-dimensional (SPDE) settings.

- The development of high-performance multilevel Monte Carlo methods leveraging the established regularity and stability.

- Analysis under weaker assumptions or with state-dependent jump intensity.

Conclusion

The paper provides a rigorous and comprehensive account of the tamed Euler scheme for Lévy-driven SDEs with superlinear growth, establishing strong convergence, temporal-spatial regularity, stability with respect to initial and time data, and full implementability. The methods and results have significant practical and theoretical implications for high-dimensional stochastic simulation and stochastic numerics involving jumps, broadening the reliable algorithmic repertoire for SDEs beyond the globally Lipschitz regime.