- The paper provides an explicit solution that characterizes the LOMV portfolio via KKT conditions and identifies its active asset set.

- It introduces a fast computational criterion for active set selection in one-factor models with mixed-sign betas.

- The study reveals high-dimensional asymptotics showing rapid sparsity and conditions under which the active ratio fails to converge.

Theoretical Characterization and Asymptotics of the Long-Only Minimum Variance Portfolio in One-Factor Markets

This work rigorously investigates the characterization and high-dimensional asymptotics of the long-only minimum variance (LOMV) portfolio within the context of a one-factor covariance model. Unlike the classic global minimum variance (GMV) solution, which allows both positive and negative (long/short) positions and is analytically tractable due to the unconstrained quadratic program structure, the LOMV introduces binding non-negativity constraints on asset weights. The presence of these constraints fundamentally alters the sparsity and diversification profile of the resulting portfolios and makes the active set identification nontrivial, especially in large p regimes with potentially mixed-sign factor loadings (“betas”). The study fills a gap left open by prior literature on the generality of mixed-sign betas and asymptotic active set characterization.

Explicit Solution for the LOMV in One-Factor Models

The authors first generalize the explicit construction for the LOMV under arbitrary positive definite covariance, leveraging the Karush-Kuhn-Tucker (KKT) conditions to show that the LOMV solution on the active set K coincides with the unconstrained GMV solution restricted to those assets. However, the crux is the selection of K, i.e., indices of positive weights.

For the single-factor model with

Σ=σ2ββ⊤+Δ

with arbitrary (mixed-sign) βi, the work provides an explicit, computational criterion: Letting R1=σ21 and recursively

Ri=Ri−1+δi−12βi−1(βi−1−βi),

the active set is the largest contiguous group {1,…,ℓ} for which Ri>0. The monotonicity properties of Ri ensure this is well-defined, and in practical terms, K0 can be rapidly searched (e.g., bisection, K1) for large K2.

This resolves the open problem posed in Qi (2021) regarding portfolios with mixed-sign betas, extending prior results which either imposed positivity assumptions (CST 2011; Qi 2021) or lacked constructive methods.

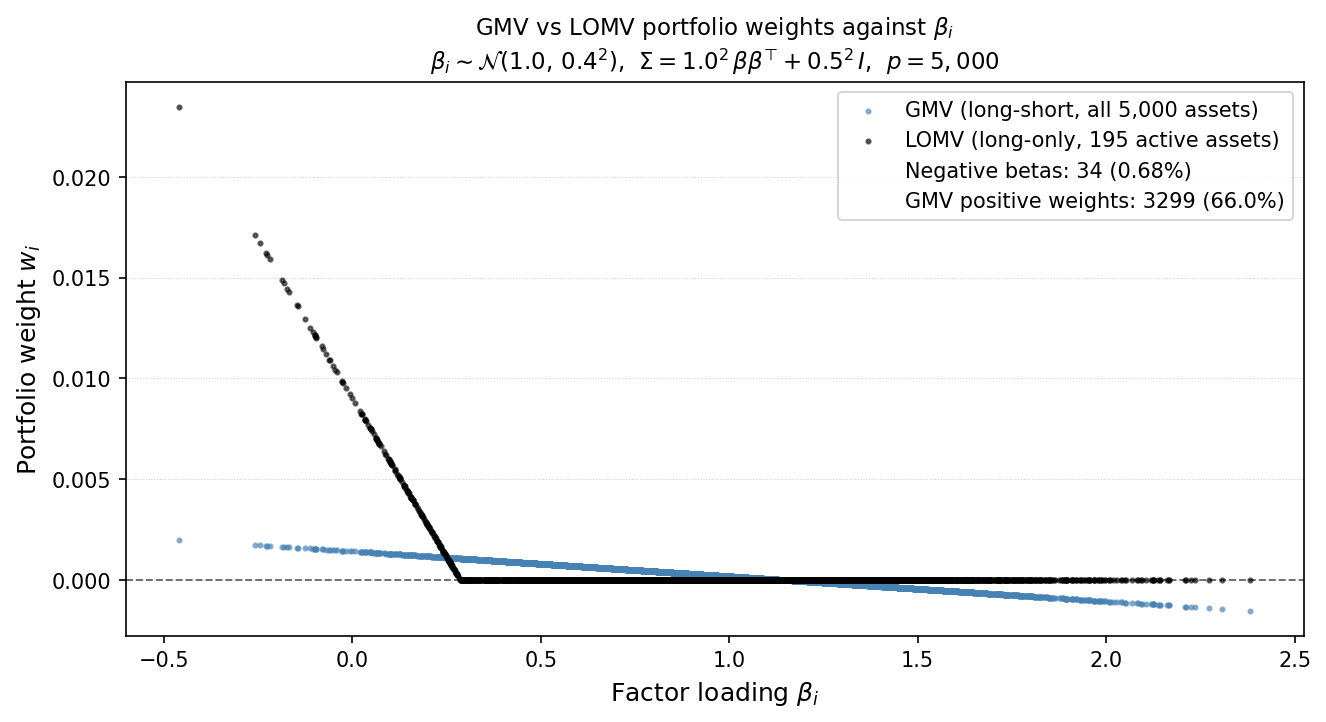

Figure 1: Comparison of long-short (blue) and long-only (black) minimum variance portfolio weights versus beta for K3 assets.

In (Figure 1), the sparsity-inducing effect of the long-only constraint is illustrated: under a normal beta distribution, the LOMV portfolio concentrates all weight on a small subset of assets with the lowest betas (including those with negative beta), whereas the GMV portfolio allocates positive weights much more broadly.

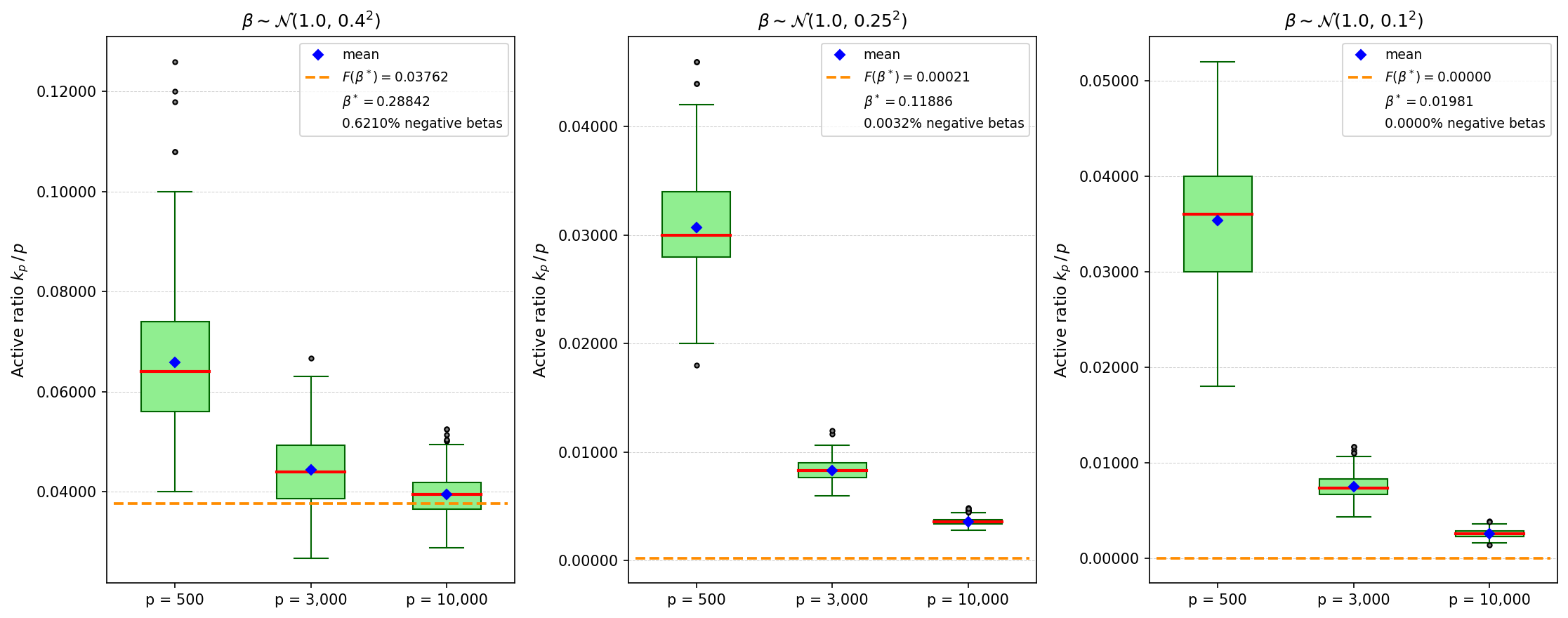

High-Dimensional Asymptotics and Active Set Proportion

In the high-dimensional limit (K4), the study investigates the "active ratio", K5, where K6 is the number of nonzero weights in the LOMV portfolio for size K7. When K8 are iid from a distribution K9, it is proven that under mild moment and regularity conditions, K0 converges almost surely to K1, where K2 is the positive root of the integral equation

K3

Continuity properties and explicit expressions for K4 lead to a sharp trichotomy of possible asymptotic regimes:

- Mixed-sign betas, positive mean: K5 unless K6 is an atom of K7 (in which case the limit does not exist and oscillates on the atom’s mass band).

- All non-negative betas: K8 unless K9 has atomic mass at its minimum support.

- All negative betas, zero mean: Σ=σ2ββ⊤+Δ0.

This result quantifies the interplay between systematic exposure in the asset universe and the sparsity implicit in long-only risk minimization.

Figure 2: Empirical distribution of Σ=σ2ββ⊤+Δ1 for LOMV with Normal beta distribution, illustrating the convergence to its theoretical limit as Σ=σ2ββ⊤+Δ2 grows.

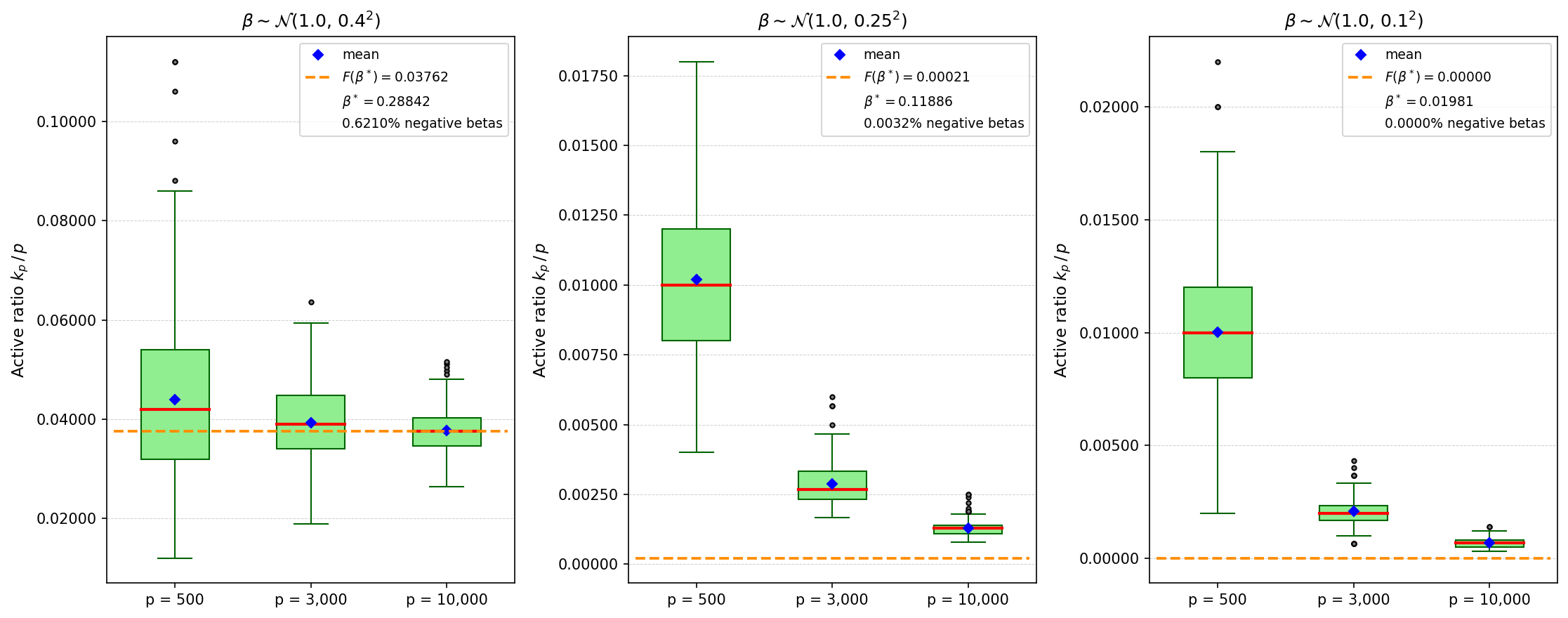

Quantitative Bounds and Rate of Decay

A major theoretical contribution is the formal rate at which the active set vanishes as the prevalence of non-positive betas decreases. Provided mild moment and concentration bounds on Σ=σ2ββ⊤+Δ3, if the probability Σ=σ2ββ⊤+Δ4 that Σ=σ2ββ⊤+Δ5 vanishes, the limiting active ratio satisfies Σ=σ2ββ⊤+Δ6. Thus, for asset universes with almost all positive market exposure, the LOMV portfolio becomes extremely sparse.

Figure 3: Distribution of Σ=σ2ββ⊤+Δ7 under decreasing negative-beta mass, visualizing rapid sparsification predicted by the Σ=σ2ββ⊤+Δ8 rate.

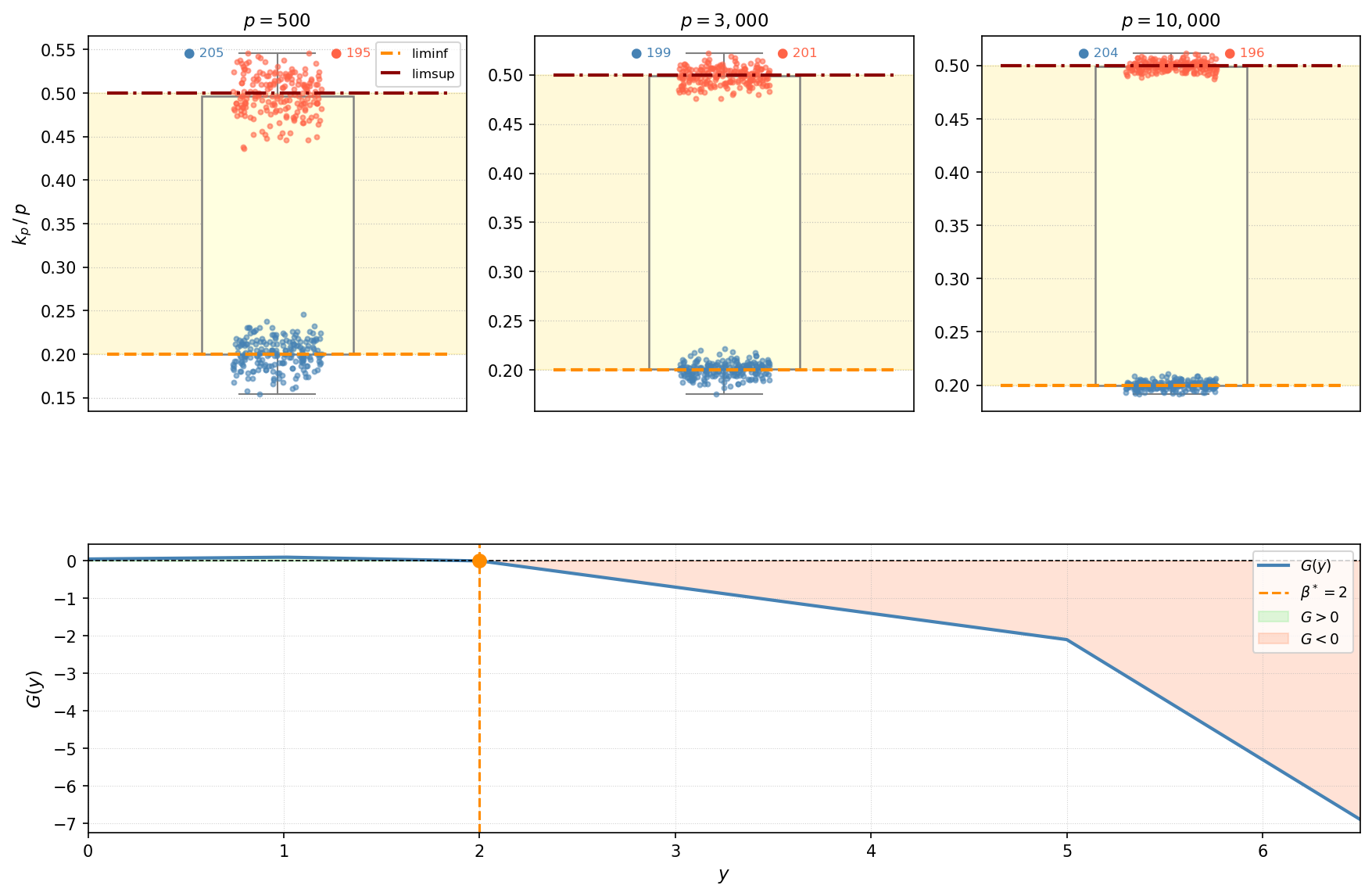

Non-Convergence Phenomenon

The work also constructs and analyzes "pathological" cases in which the limiting active ratio does not exist. If the distribution Σ=σ2ββ⊤+Δ9 has an atom at the critical threshold βi0, βi1 can oscillate between βi2 and βi3, as shown both analytically and via simulation. Such scenarios are statistically rare but impossible to exclude in discrete or empirical universes.

Figure 4: Simulation example demonstrating non-convergence of βi4 when βi5 has an atom at βi6. Two modes correspond to realizations where all, or none, of the atom's block is active.

Implications and Future Directions

Practical implications: The results provide operationally efficient algorithms for constructing the LOMV portfolio in high-dimensional settings, especially relevant to index fund design, risk premia strategies, and regulatory compliance where shorting is prohibited. The sparsity induced by the long-only constraints suggests that naive expectations of diversification are not met under factor-dominant regimes—most assets receive zero allocations unless sufficiently de-risked by negative betas.

Theoretical implications: The precise relationship between the distributional properties of factor exposures and sparsity/selection in constrained quadratic optimization deepens understanding of convex program behavior under linear inequality constraints. These asymptotics may inform regularization strategies in high-dimensional factor models and motivate further study of alternative shrinkage estimators and relaxation of covariance assumptions.

Future research: Addressing extensions to multi-factor models, adaptive shrinkage for empirical covariance estimation, and robustness to sample estimation error remain outstanding. The general methodology for active set identification may translate to broader classes of portfolio and signal selection problems under convex constraints.

Conclusion

The paper provides an explicit, computationally efficient solution for the LOMV portfolio under a one-factor model with mixed-sign betas and delivers a rigorous asymptotic theory for the active ratio in large universes. The active set is driven by the lower tail of the beta distribution, and, in most realistic regimes, sparsifies rapidly as negative betas vanish. The results clarify both the structure and the limitations of long-only minimum variance allocations relative to unconstrained benchmarks and establish a foundation for further work in high-dimensional constrained optimization in finance and statistics.