- The paper introduces a novel framework using sequential conformal recalibration to align next-day VaR with a target exceedance rate.

- It combines conditional quantile regression and an adaptive corrective layer to address marking frictions and manage portfolio-level tail risk.

- Empirical results on SPX option data demonstrate significant improvements in risk coverage, particularly during turbulent market conditions.

Adaptive VaR Control in Option Portfolios under Marking Frictions

Introduction and Motivation

Short-horizon risk control for derivatives portfolios, especially standardized option books, remains operationally and theoretically challenging due to next-day valuation frictions and the complex, portfolio-level nature of tail risk. The paper "Adaptive VaR Control for Standardized Option Books under Marking Frictions" (2604.03499) introduces a new framework for controlling Value-at-Risk (VaR) for standardized option portfolios under practical data limitations, notably next-day marking frictions. This framework targets precise, exposure-controlled books and links predictions directly to realized, normalized losses, allowing for rigorous coverage evaluation under real-world market conditions.

The central objective is to estimate, for each day and each book, a threshold qt,α(b) such that the probability of next-day normalized loss Yt+1(b) exceeding qt,α(b) is at most α, controlling for sharp failures in downside risk management at a specified quantile (typically α=0.10). The architecture departs from historical approaches by directly formulating the risk target at the portfolio level, rather than at the contract or return series level. The loss of a standardized option book depends jointly on leg selection, spot hedging, and, crucially, on the operational ability to mark each leg on the next day. The paper formalizes and quantifies the impact of these marking frictions, providing explicit distortion bounds for marking errors and demonstrating empirically that book-level VaR cannot be identified purely from contract-level risk estimates due to the necessity of capturing joint tail dependence.

The forecasting pipeline integrates conditional quantile regression (with LightGBM as the main engine) and introduces a sequential conformal recalibration layer to adaptively correct for regime shifts and distributional changes. This is operationalized through a one-sided, exponentially-weighted buffer added to the reference quantile levels, recalibrated daily using recent residuals. This arrangement provides approximate one-step exceedance control, giving a theoretically grounded, practical guarantee that the next-day exceedance rate aligns with the target α up to explicitly characterized approximation errors.

A hierarchy of marking approaches—exact match, contract matching, moneyness interpolation, and nearest-neighbor fallback—is enforced to address the unavailability of direct next-day contract quotes in real data, ensuring operational feasibility while keeping the impact of marking distortions controlled and transparent.

Empirical Study: Data, Portfolios, and Coverage Results

The empirical evaluation uses over seven years of SPX option data (2018–2025), constructing three economically representative books: a 30-day at-the-money straddle, a 25-delta risk reversal, and a 25d/10d short put spread. Each book’s normalized loss is defined relative to the total premium, with spot hedging included to neutralize unwanted deltas. The out-of-sample panel size varies from roughly 1,000 to over 1,100 per book.

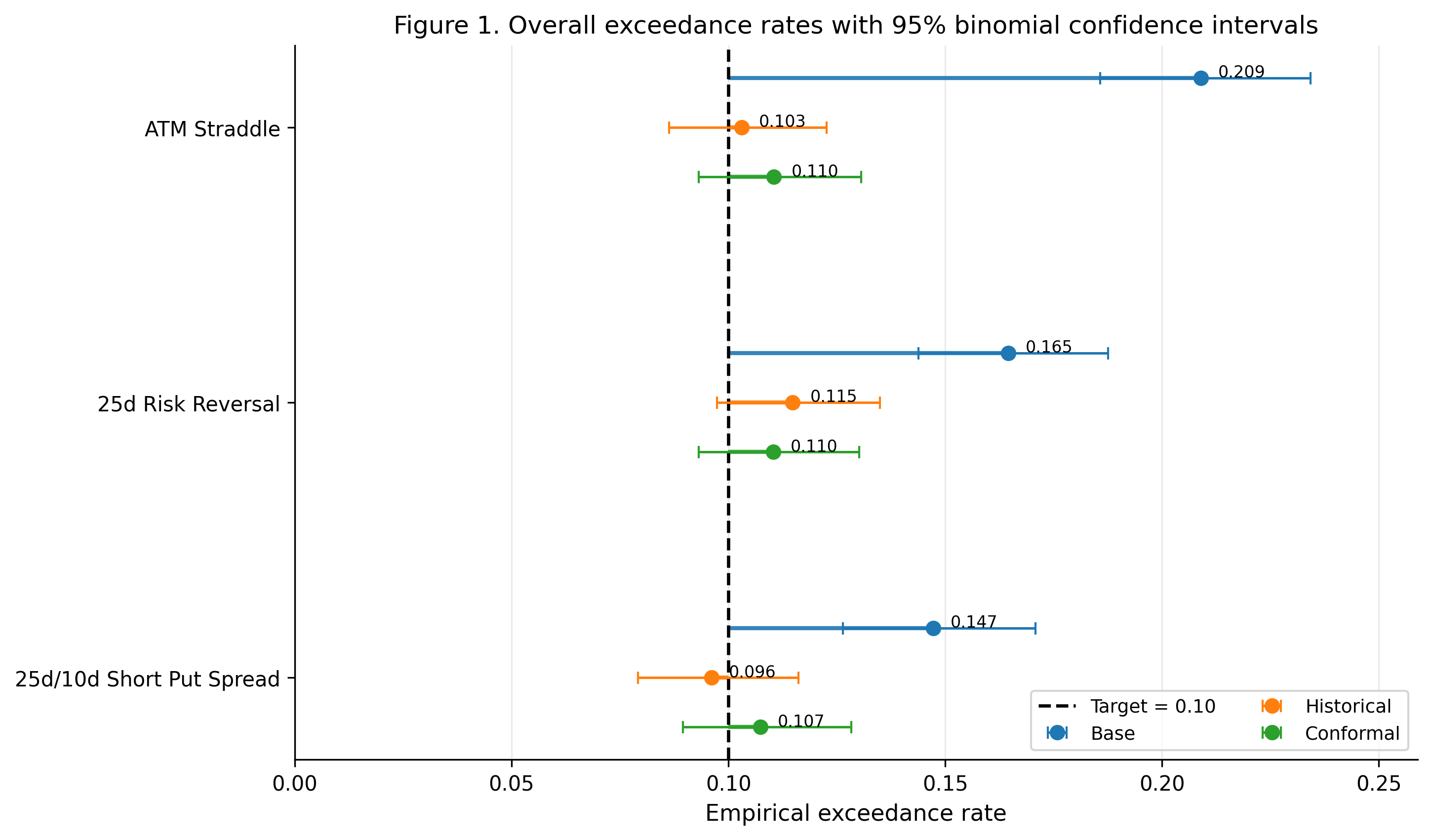

The raw quantile regression baseline significantly underestimates downside risk, with observed empirical exceedance rates of 0.209 (ATM straddle), 0.165 (risk reversal), and 0.147 (short put spread), all well above the 0.10 target. In sharp contrast, the conformal recalibration procedure brings exceedance rates close to target, at 0.110, 0.101, and 0.107, respectively.

Figure 1: Overall exceedance rates with 95% binomial confidence intervals for all methods and books; the dashed line indicates the nominal 0.10 level.

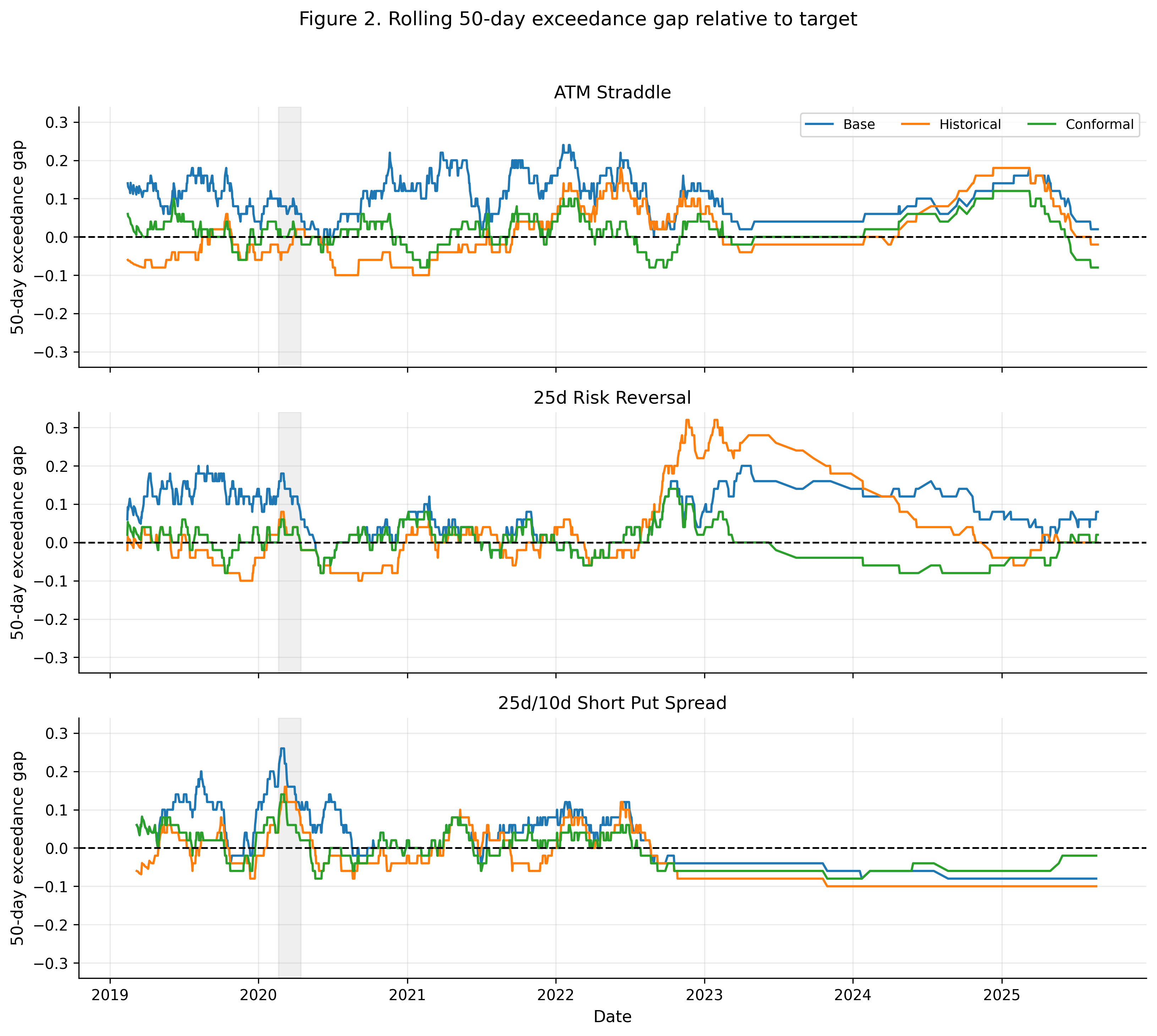

Rolling window analysis highlights the role of the conformal layer in stabilizing local tail coverage, reducing maximum 50-day rolling exceedances and eliminating persistent undercoverage during turbulent periods and market crises.

Figure 2: Rolling 50-day exceedance gaps relative to the 10% target, illustrating improved local calibration and resilience during stress periods.

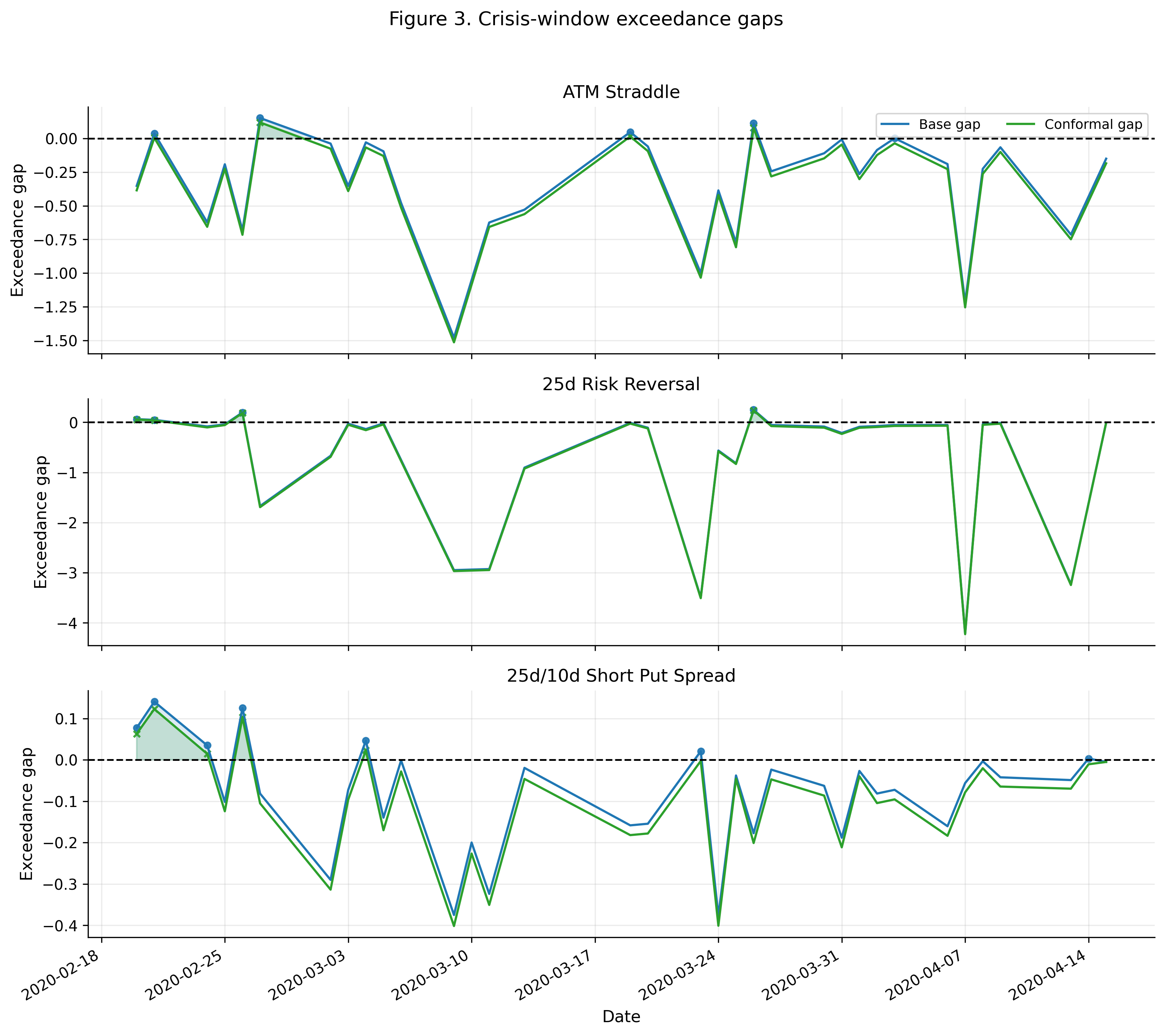

In the COVID-19 crisis window, the conformal approach reduces exceedance rates in the straddle and put spread books by more than three percentage points, while base models continue to show elevated losses above the nominal VaR.

Figure 3: Daily crisis-window exceedance gaps, showing substantial suppression of large positive excursions under the adaptive conformal rule.

Robustness and Operational Diagnostics

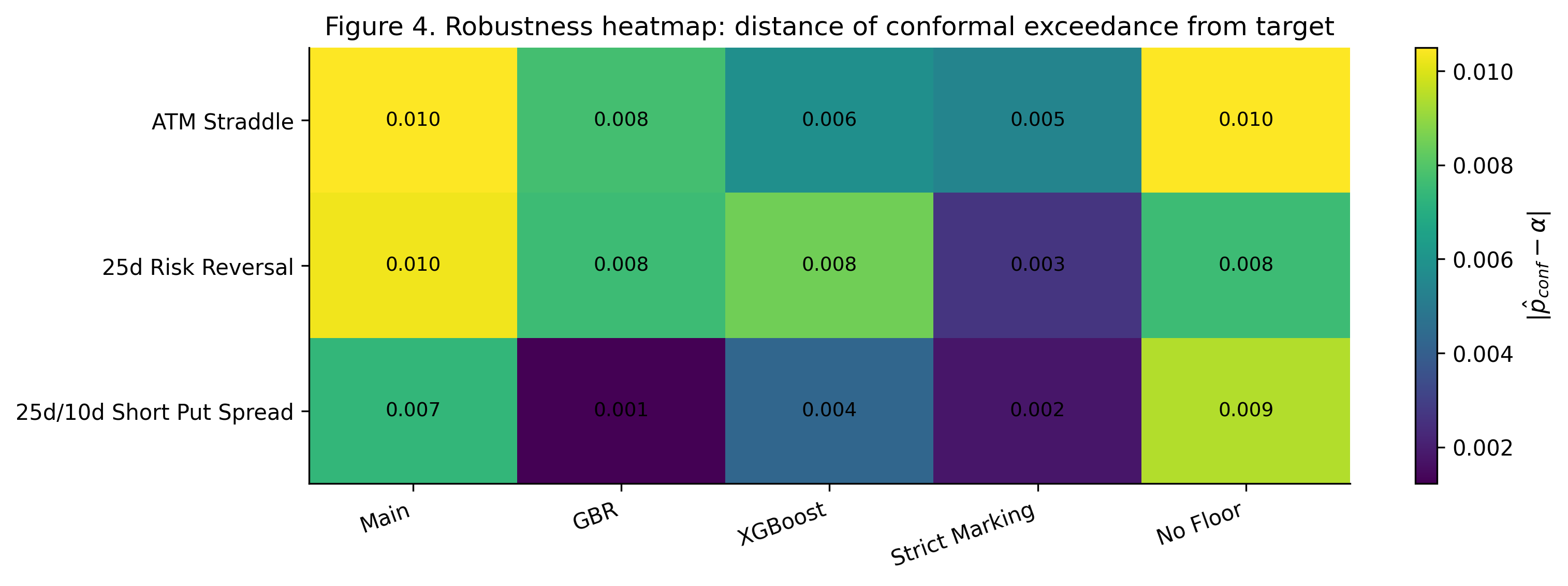

Robustness tests against alternative base learners (GBR, XGBoost), stricter marking regimes, and removal of the floor constraint yield conformal exceedance rates that remain tightly clustered around the nominal value, indicating that the risk control improvement is not contingent on specific model or marking choices.

Figure 4: Calibration distances across robustness specifications, demonstrating tight control over empirical exceedance in all configurations.

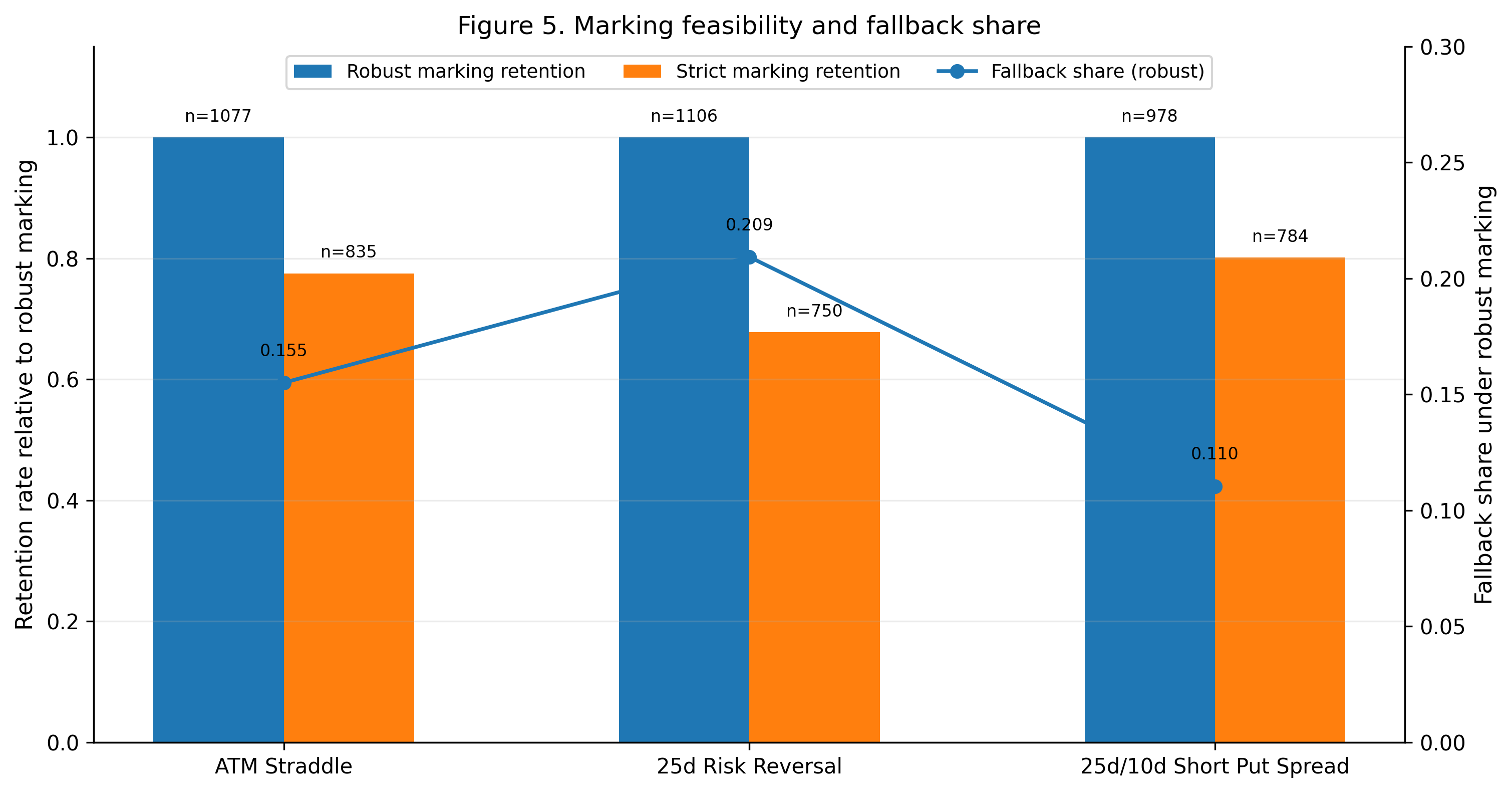

Operational feasibility assessment shows that robust marking increases the usable sample by over 30% compared to strict marking, crucial for maintaining coverage in the presence of real-world data gaps. Fallback mode usage under this hierarchy is moderate and well characterized.

Figure 5: Comparison of usable sample retention and fallback share between robust and strict next-day marking protocols.

Theoretical and Practical Implications

This research establishes a practical and theoretically principled mechanism for adaptive short-horizon risk control in nonlinear, standardized option portfolios. By anchoring forecasts to normalized book losses and using online conformal recalibration, it overcomes both data-driven marking limitations and the inherent nonstationarity of financial markets. The approach enables more credible capital allocation, limit setting, and stress analysis for derivatives desks and risk managers.

Theoretically, the findings clarify that portfolio-level VaR for options portfolios is a joint-distribution property not identifiable from contract-level marginal risk alone, motivating risk architecture that is structurally compatible with exposure composition and operational marking realities.

Future Directions

Key avenues for future research include extending the methodology to more complex, multi-asset or path-dependent derivatives portfolios; integrating alternative sequential recalibration approaches (e.g., betting-based conformal or online risk-control frameworks); and exploring stress-specific forecast design under extreme illiquidity or correlated marking failures. Deeper integration with margin and capital policy and the adaptation to regime-aware risk management pipelines are also warranted.

Conclusion

The sequential conformal recalibration framework described in this paper restores the credibility of daily VaR for standardized option portfolios under demanding marking and nonstationarity conditions. The empirical evidence shows marked improvement in both global and local tail risk control, robustness across model and data choices, and practical operational feasibility. These results substantiate the premise that risk control in real option books must be anchored not only to statistical VaR models but to portfolio-level, operationally implementable targets, with explicit sequential recalibration to match evolving market regimes.