- The paper demonstrates that integrating option-implied, rough volatility estimators into the HAR model significantly improves realized volatility forecasts for the S&P 500 index.

- It implements a deep learning surrogate to overcome the computational challenges in calibrating the rough Heston model, ensuring efficient model inference.

- Out-of-sample and multi-horizon tests confirm the rough volatility model’s superiority over classical SV models and the VIX index in forecasting accuracy.

Options-Driven Realized Volatility Forecasting via Rough Volatility Models

Introduction

This study rigorously investigates the incremental informational gains of incorporating option-implied, model-based spot volatility estimates derived from rough volatility models, particularly the rough Heston formulation, into realized volatility forecasting frameworks. The focal point is augmenting the Heterogeneous Autoregressive (HAR) model with forward-looking spot volatility extracted from traded options, juxtaposed against benchmarks based on classical stochastic volatility (SV) models (Heston, Bates, SVCJ) and the non-parametric VIX index. The authors further resolve the prohibitive computational overhead inherent in rough volatility estimation by deploying a deep learning surrogate for the option pricing function.

Data and Empirical Realized Volatility Construction

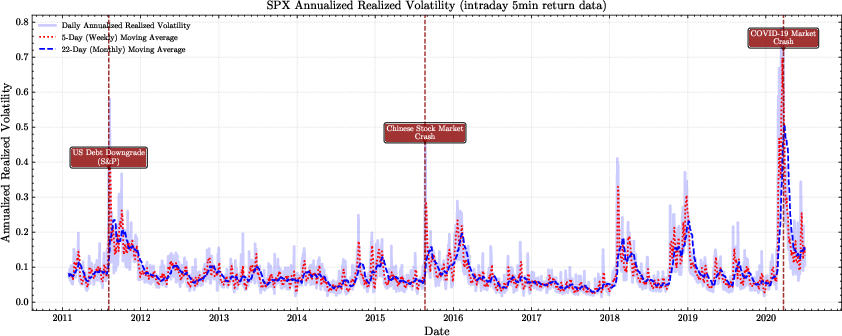

The analysis utilizes high-frequency intraday (5-minute) returns on the S&P 500 over an extensive period, with realized volatility (RV) computed as the sum of squared returns. The use of 5-minute sampling is justified, following [liu2015does], as optimal for signal extraction while mitigating microstructure noise.

Figure 1: Time series of daily realized volatility for S&P 500 using high-frequency intraday returns.

The descriptive statistics of RV, along with its log-transformed version to reduce skewness, set the empirical foundation for out-of-sample forecasting and model validation. The temporal clustering and sustained spikes within RV clearly motivate the need for richer volatility dynamics than classical Markovian SV models can accommodate.

Model-Based Spot Volatility Estimation from Options

Rough Heston Model and Implementation

The rough Heston model imposes a non-Markovian, fractional structure on the instantaneous variance process. This theoretical innovation, rooted in [gatheral2018volatility], enables the model to encode the roughness empirically observed in realized and implied volatility time series. Given computational constraints—the characteristic function for the rough Heston model involves fractional Riccati equations—the authors pursue a tractable Markovian multi-factor approximation, further accelerated via a deep neural network surrogate trained on synthetic option price panels.

Deep Learning Surrogate for Option Pricing

A multilayer perceptron is constructed to approximate the mapping from model parameters and contract attributes to European option prices. This surrogate achieves sufficiently low mean absolute percentage error on out-of-sample pricing tasks, thus serving as a drop-in replacement for conventional, computationally burdensome pricing engines.

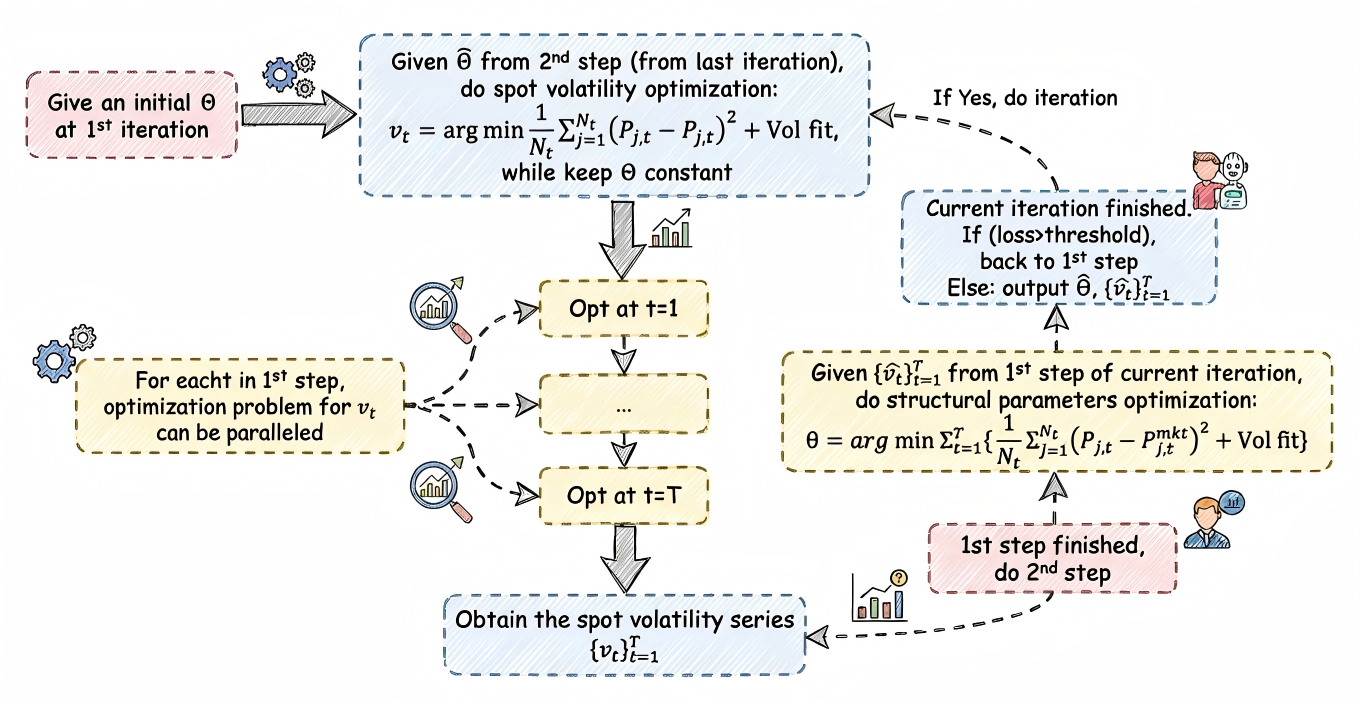

Iterative Two-Step Parametric Inference

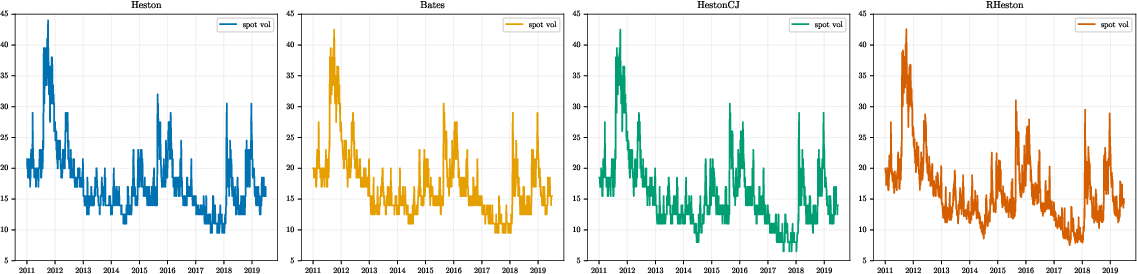

To estimate latent spot volatility, the study adopts the penalized nonlinear least squares framework of [andersen2015parametric]. This involves an alternating procedure: fixing parameters to estimate the latent Vt time series and then updating parameters conditioned on the inferred states, leveraging both cross-sectional and time-series information. Out-of-sample robustness is ensured by restricting parameter reestimation to annual windows. The resulting spot volatility series for each SV model and the rough Heston model display persistent positive skewness and volatility clustering.

Figure 2: Flowchart of the iterative two-step parametric inference procedure for extracting model-based spot volatility from option panels.

Figure 3: Daily spot volatility estimators derived under Heston, Bates, SVCJ, and rough Heston models.

Integration with HAR(-X) Volatility Forecasting Framework

Model Specifications

The standard HAR-RV model is extended to incorporate exogenous volatility information: the VIX (HAR-RV-VIX) or model-inferred spot volatilities from Heston-like and rough Heston models (HAR-RV-SV, HAR-RV-RHeston). Each augmented model is specified with the exogenous variable entering contemporaneously to the lagged multi-horizon realized volatility predictors.

In-Sample Results

All exogenous-augmented HAR(X) variants markedly increase the adjusted R2 relative to the benchmark HAR-RV. The HAR-RV-RHeston exhibits the greatest explanatory power, with the spot volatility from the rough Heston model yielding the most significant and economically interpretable coefficient.

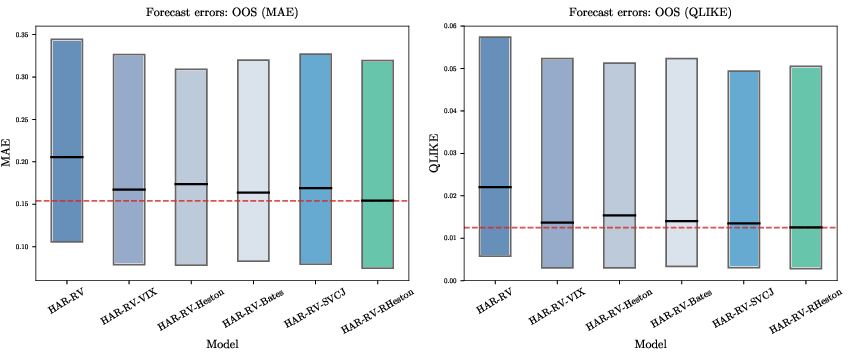

Out-of-Sample Forecasting

Forecast accuracy is benchmarked across multiple loss functions (MAE, RMSE, QLIKE) and mean directional accuracy (MDA). The HAR-RV-RHeston model achieves the lowest errors and highest MDA, demonstrating a clear performance hierarchy in which rough volatility-informed predictors dominate VIX and traditional SV paths.

Figure 4: Boxplots of MAE and QLIKE forecast errors for competing volatility models, highlighting the reduced median and outlier dispersion of HAR-RV-RHeston.

Diebold-Mariano tests confirm the statistical significance of these improvements, with HAR-RV-RHeston consistently outperforming both non-parametric (VIX) and classical SV-augmented HAR extensions.

Multi-Horizon Forecast Efficacy

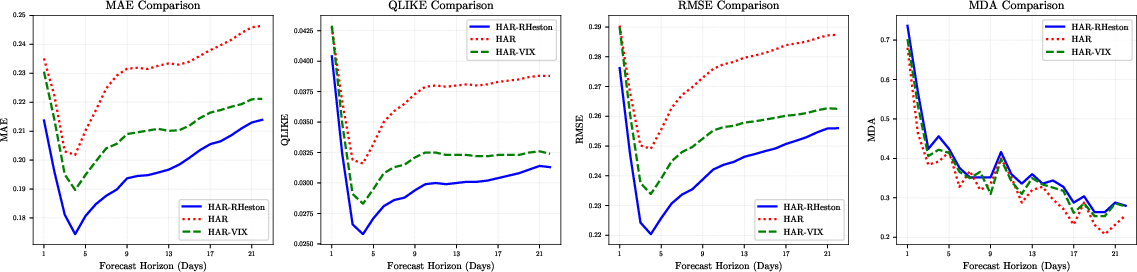

Extending the analysis to multi-period horizons (1–22 days), the HAR-RV-RHeston model maintains superior performance across all error metrics and most directional accuracy evaluations, indicating the persistence of the informational content in rough volatility even as prediction horizons expand.

Figure 5: Comparative multi-horizon (1–22 days ahead) forecasting performance for HAR-RV, HAR-RV-VIX, and HAR-RV-RHeston using MAE, QLIKE, RMSE, and MDA.

Theoretical and Practical Implications

The findings have several direct implications:

- Informational Efficiency of Options: The evidence decisively supports the inclusion of option-implied, model-based spot volatility as a critical predictor in volatility dynamics, in line with the forward-looking efficiency hypothesis.

- Superiority of Rough Volatility: The outperformance of rough Heston-based estimators validates the empirical necessity of roughness in modeling volatility as seen in realized and implied volatility time series.

- Machine Learning in Quantitative Finance: The deployment of deep learning surrogates to facilitate scalable model calibration points the way for integration of statistical learning with stochastic model-based inference, especially in high-dimensional, non-affine settings.

Future Directions

The study recognizes the potential for even more expressive models, specifically the quadratic rough Heston model [gatheral2020quadratic], which can achieve joint calibration on both SPX and VIX options. The main limitation is computational, but further advances in machine learning-based surrogates, specialized numerical solvers, and GPU acceleration are expected to enable more routine use of such advanced models for both calibration and forecasting.

Conclusion

This work affirms the incremental value of option-implied spot volatility estimators, especially those derived from rough volatility models, in realized volatility forecasting. By expertly combining advanced econometric inference with scalable deep learning surrogates, the authors achieve significant gains in forecast accuracy—both in-sample and out-of-sample, and across short and long horizons—relative to approaches based on classical information or the VIX index. The results motivate continued integration of rough volatility dynamics and machine learning techniques for both academic research and quantitative investment practice.

Reference: "On options-driven realized volatility forecasting: Information gains via rough volatility model" (2604.02743).