Do Prediction Markets Forecast Cryptocurrency Volatility? Evidence from Kalshi Macro Contracts

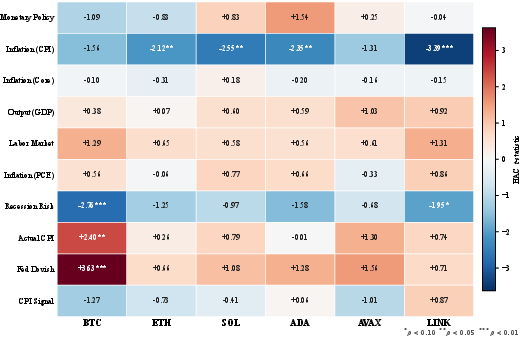

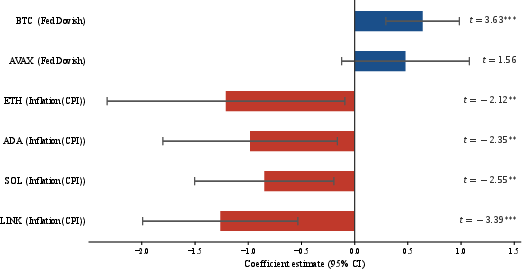

Abstract: Daily probability changes in Kalshi macro prediction markets forecast cryptocurrency realized volatility through two distinct channels. The monetary policy channel, measured by Fed rate repricing on KXFED contracts, predicts Bitcoin volatility in sample with t = 3.63 and p < 0.001 but exhibits regime dependence tied to the 2024-2025 rate-cutting cycle. The recession risk signal from KXRECSSNBER proves more stable out of sample, delivering an MSFE ratio of 0.979 with Clark-West p = 0.020. The inflation channel, measured by CPI repricing on KXCPI contracts, predicts altcoin volatility for Ethereum, Solana, Cardano, and Chainlink with t-statistics ranging from -2.1 to -3.4 and out-of-sample gains for Ethereum at MSFE = 0.959 with p = 0.010 and Solana at p = 0.048. Both the Bitcoin--Fed-dovish and Chainlink--CPI specifications survive Benjamini-Hochberg correction at q = 0.05. Orthogonalization and baseline comparisons against Fed Funds futures, Treasury yields, and the Deribit implied volatility index confirm that these signals carry information not embedded in conventional financial instruments. The sample covers ten Kalshi event series and six cryptocurrency assets over January 2023 to March 2026.

Paper Prompts

Sign up for free to create and run prompts on this paper using GPT-5.

Top Community Prompts

Explain it Like I'm 14

What is this paper about?

This paper asks a simple question: can “prediction markets” help us forecast how wild (or calm) cryptocurrency prices will be next week? It looks at prices from Kalshi, a U.S. regulated exchange where people trade on future events like Federal Reserve rate decisions or inflation. The authors test whether daily changes in those prediction market probabilities can predict the near‑term ups and downs (volatility) of Bitcoin and several other coins.

What questions did the researchers ask?

- Do daily shifts in prediction market odds (from Kalshi) tell us something about next‑week crypto volatility that regular markets (like bonds, Fed futures, or options) don’t already tell us?

- Which kinds of macro news matter for which coins? For example, do interest‑rate expectations matter more for Bitcoin, while inflation news matters more for smaller coins?

How did they study it?

Think of a prediction market like a weather forecast for the economy, updated every day. The price of a Kalshi contract is the market’s best guess (as a probability) that an event will happen. When the price moves, it means the crowd has updated its beliefs.

Here’s the approach, in everyday terms:

- Signals from prediction markets

- The authors track daily changes in the odds for several macro topics:

- Federal Reserve interest rates (monetary policy)

- Inflation (CPI)

- Recession risk (whether the U.S. will be declared in recession)

- They summarize each day’s move by taking a volume‑weighted average change for each topic (bigger trades count more).

- They mostly use the size of the change (how big the repricing was), not the direction. Two exceptions use direction:

- “Fed‑dovish” means odds moved toward lower interest rates.

- CPI and NFP (jobs) also have directional versions, but the main CPI results use the size of the move.

- What they try to predict

- For six coins (Bitcoin, Ethereum, Solana, Cardano, Avalanche, Chainlink), they try to predict next week’s “realized volatility,” which is like measuring how bumpy the ride actually is over the next five trading days.

- The forecasting setup

- Start with a standard “HAR” model that predicts volatility from recent volatility patterns (yesterday, last week, last month). Think of HAR as “use the recent bounciness to guess tomorrow’s bounciness.”

- Add common market controls: VIX (stock market fear), the U.S. dollar (DXY), and the S&P 500.

- Then add the Kalshi signal and see if it improves the forecast.

- Compare against “regular” instruments: Fed Funds futures, Treasury yields, and crypto options volatility (Deribit DVOL) to check if Kalshi really adds new information.

- Making sure the results are solid

- They do “out‑of‑sample” tests: train on earlier data, then test on later data—like studying for a test and then taking a new one.

- They correct for many simultaneous tests (to avoid false alarms) and use robust statistics to handle overlapping days and noisy data.

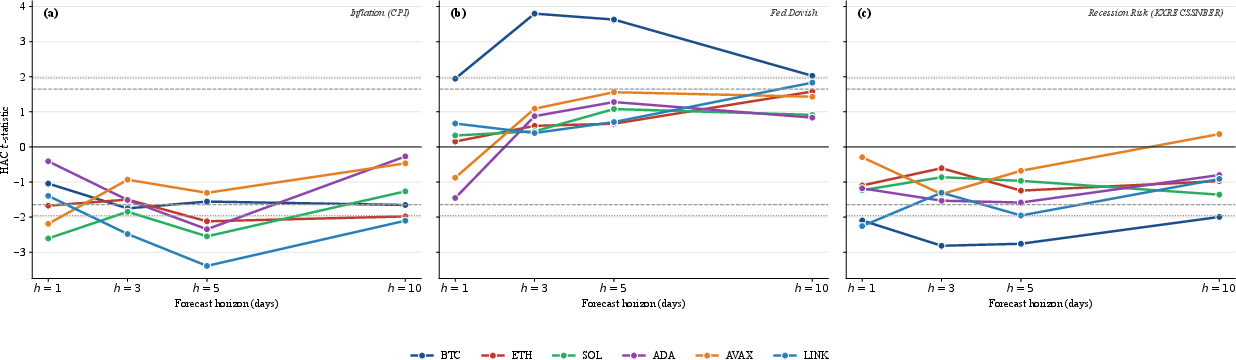

- They also check timing (lead–lag) to see if crypto moves first (it doesn’t for the Fed signal) and test that Kalshi signals aren’t just copies of bond or futures market information (they aren’t).

- Data

- Period: January 2023 to March 2026.

- Assets: BTC, ETH, SOL, ADA, AVAX, LINK.

- Kalshi series: about ten macro topics, with best coverage for Fed policy, CPI, and recession.

What did they discover?

Big picture: different kinds of macro news matter for different coins.

- Bitcoin and interest rates (the Fed)

- When Kalshi odds shift toward lower future interest rates (a “dovish” move), Bitcoin’s next‑week volatility tends to rise.

- This was very strong inside the sample, especially during the 2024–2025 period when the Fed was cutting rates. Outside that period, the effect faded. In other words, it’s “regime dependent”: most useful when rate expectations are actively changing.

- Bitcoin and recession odds

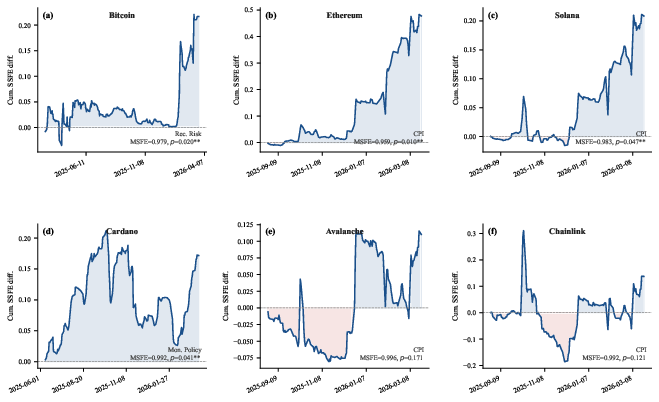

- A steadier signal came from Kalshi’s recession risk market. Rising or falling recession odds helped improve out‑of‑sample forecasts for Bitcoin’s volatility, even more reliably than the Fed signal across the full test period.

- Altcoins and inflation (CPI)

- For Ethereum, Solana, Cardano, and Chainlink, bigger day‑to‑day changes in CPI odds predicted lower volatility in the following week.

- Why lower? Because big shifts in CPI odds usually happen around inflation report days. Once the report is out, uncertainty gets resolved, and the market calms down.

- This effect was strongest and most consistent for ETH, SOL, and LINK, and it showed real forecasting improvement out of sample for ETH and SOL. Avalanche didn’t show a clear pattern.

- Not just copying other markets

- The Kalshi signals carried information that wasn’t already in Fed Funds futures, 10‑year Treasuries, the stock market, the dollar, or even crypto options implied volatility.

- In head‑to‑head tests, the Kalshi signals kept their predictive power while the conventional benchmarks did not.

- How big are the improvements?

- The gains are modest but meaningful for such a noisy market: about 2–4% better mean squared forecast error in the best pairs (e.g., BTC with recession risk; ETH and SOL with CPI).

- For statistics fans: these passed conservative “Clark–West” tests and, in some cases, multiple‑testing correction.

Why does this matter?

- For investors and risk managers

- Better near‑term volatility forecasts help with position sizing: take smaller positions when volatility is predicted to rise, and larger when it’s predicted to fall.

- Around big CPI repricing days, altcoin options might be overpriced if traders don’t account for the likely post‑report calming. That can matter for strategies like selling straddles (with care about costs and risks).

- For understanding crypto markets

- Crypto doesn’t move on just one kind of macro news. Bitcoin seems more tied to interest‑rate and recession expectations, while several altcoins are more sensitive to inflation news.

- Prediction markets provide a continuous, day‑by‑day macro “thermometer,” filling the gap between official data releases.

- For future research and policy

- The Fed‑related effect depends on the rate‑cutting period studied; longer samples across more cycles are needed to confirm how stable it is.

- Intraday data could pin down timing even better.

- Comparing with other event markets (like Polymarket) could test whether these results generalize beyond Kalshi.

In short: carefully measured daily swings in prediction market odds—especially for the Fed, inflation, and recession—help forecast next‑week crypto volatility. Bitcoin reacts most to interest rates and recession risk; several altcoins react most to inflation. These signals add information beyond traditional finance tools, and they’re most useful during periods when macro expectations are actively shifting.

Knowledge Gaps

Knowledge gaps, limitations, and open questions

Below is a focused list of what remains missing, uncertain, or unexplored, framed to guide follow-on research.

- External validity across regimes: The sample (2023–2026) spans a single inflation episode and a rate-cutting cycle; it is unknown whether the documented channels persist across tightening cycles, disinflationary periods, and low-volatility regimes.

- Longer horizons and stability: Effects are strongest at 3–5 days; there is no systematic assessment of stability across 10–30 day horizons, structural breaks, or parameter drift via rolling/regime-switching models.

- Identification of mechanisms: The paper posits institutional vs retail investor channels but lacks participant-level or venue-level flow data to test whether the same agents trade on Kalshi and in crypto markets.

- Intraday timing of information flow: Daily closes obscure within-day lead–lag; high-frequency event-time analysis around FOMC/CPI/contract repricing could pin down causality and transmission speed.

- Directionality of CPI surprises: Results rely on absolute CPI repricing; the asymmetric impact of positive vs negative inflation repricing on altcoin volatility is not established.

- Alternative signal constructions: Only volume-weighted daily probability changes are tested; unexamined are open-interest-weighted changes, entropy/KL-divergence across thresholds, tail-probability shifts, signed jumps, or microstructure-informed de-noising.

- Risk-neutral vs physical probabilities: The claim that risk premia “cancel in first differences” is untested; quantifying time-varying risk premia in Kalshi prices and their impact on the signal would strengthen inference.

- Microstructure noise in Kalshi prices: Absent bid–ask quotes and depth, the extent to which closing-price noise contaminates Δp signals (especially in thin trading) is unknown; robustness to microstructure filters is untested.

- Liquidity-state dependence: The predictive content may vary with Kalshi and crypto liquidity (volume, spreads, OI); formal interactions with liquidity measures are not estimated.

- Cross-platform generalizability: Evidence is limited to Kalshi; replication on Polymarket, PredictIt, CME event futures, and European macro event markets is needed.

- Global macro drivers: Only U.S. macro contracts are considered; the role of ECB, BoE, BoJ, China macro, and global PMIs for crypto volatility remains unexplored.

- Broader asset coverage: Results are for six large assets; extension to mid-cap altcoins, DeFi tokens, stablecoins, and cross-exchange-traded tokens could test breadth and heterogeneity.

- Crypto-specific confounders: Regulatory actions (e.g., ETF approvals/denials), protocol upgrades, hacks, and halvings are not controlled; their interaction with macro repricing is unquantified.

- Covariance and spillovers: The paper focuses on univariate volatility; whether Kalshi signals forecast cross-asset covariance/correlations or systemic crypto volatility is an open question.

- Nonlinear and state-dependent effects: Thresholds, quantile regressions, and interactions with market states (e.g., DVOL level, funding rates, risk-on/off proxies) are not estimated.

- Model class diversity: HAR dominates; comparative tests with realized-kernel measures, bipower variation, semivariances, MIDAS-RV, HEAVY, and machine learning (e.g., LASSO/GBMs with interactions) are absent.

- Loss function robustness: OOS evaluation uses MSFE and CW; results under QLIKE, MAFE, or volatility-targeting-relevant losses (e.g., log-loss for variance) are not reported.

- Placebo and pseudo-event checks: Placebo dates or shuffled Kalshi series to gauge spurious fit are not presented; additional reality checks could bound data-snooping risk.

- Multiple-testing control beyond BH: BH is applied once; pre-registration, holdout samples, and stepwise familywise-error procedures (e.g., Romano–Wolf) could strengthen claims.

- Rolling vs expanding windows: Only expanding-window OOS is used; rolling windows and time-varying parameter models could reveal hidden regime dependence or decay.

- Tradeability and net performance: Proposed applications (vol-managed BTC, ETH options) lack full backtests with transaction costs, slippage, margin/leverage constraints, borrow/fees, and realistic execution timing.

- Options-market linkage: Direct tests of implied-minus-realized volatility around high-Kalshi CPI episodes (term structure, smile dynamics, realized variance swap proxies) are not conducted.

- Weekend/holiday handling: Excluding weekends/holidays may bias signals for 24/7 crypto; robustness to including weekends (with proxy controls) or calendar-adjusted alignment is untested.

- Alignment sensitivity: Results assume 4pm ET Kalshi close vs 7pm ET crypto close; alternative alignments and timezone-normalized intraday windows could validate the 21-hour buffer assumption.

- Error-in-variables concerns: Measurement error in Δp likely attenuates coefficients; IV or SIMEX-style corrections are not attempted.

- Event window controls for FOMC: CPI release-window dummies are tested, but similar controls for FOMC and other macro events are not reported; residual calendar effects may remain.

- Forecast combinations: The composite signal underperforms, but optimal weighting/stacking (e.g., Bayesian model averaging, elastic-net combinations) is not explored.

- Heterogeneity in exchange venues: Volatility responses may differ across centralized and decentralized venues; venue-level returns/volatility could clarify microstructure channels.

- Funding, basis, and leverage: Interactions with perpetual funding rates, spot–futures basis, and open interest (CME/Deribit/on-exchange) are not analyzed.

- Tail risk and distributional effects: Impacts on higher moments (skew, kurtosis), jump variation, and tail risk metrics (VaR/ES) are not assessed.

- Robustness to outliers: Influence diagnostics and fat-tail robust regressions (e.g., Huber, quantile) are not presented; sensitivity to extreme repricing days is unknown.

- Contract lifecycle effects: Listing/expiration dynamics and tenor mix within Kalshi series may shape Δp; lifecycle normalization or tenor-fixed effects are not modeled.

- Missing and sparse series: NFP and rate-cut series are dropped for coverage; strategies to handle sparsity (e.g., pooling across vintages, hierarchical models) remain unexplored.

- Recession-risk signal interpretation: The underlying economic content of KXRECSSNBER (hedging vs speculative OI) is speculative; decomposing signal by OI/volume cohorts could clarify.

- Reproducibility and code: Full replication materials, data cleaning logic (e.g., contract mapping, inactive days), and code availability are not detailed; this limits external validation.

- Policy shock decomposition: Monetary policy “dovish” repricing blends rate-path and information effects; decomposing via high-frequency yield curve factors (target/path/term-premium components) is not attempted.

- Cross-asset predictability: Whether Kalshi signals for one macro domain forecast volatility in related crypto sectors (e.g., DeFi vs L1s) or equities/FX/commodities is not examined.

- Economic magnitude under leverage constraints: Reported effect sizes are modest; assessing utility gains under realistic risk budgets and drawdown limits would clarify practical value.

- Survivorship and listing bias in Kalshi: Changes in contract design, tick size, or listing policy over time may affect Δp; controlling for exchange rule changes is not addressed.

Practical Applications

Immediate Applications

These applications can be deployed with current data, infrastructure, and methods, drawing directly on the paper’s validated channels (monetary policy/KXFED for BTC, recession risk/KXRECSSNBER for BTC, and CPI/KXCPI for ETH, SOL, ADA, LINK).

- Volatility-managed crypto portfolios (Sector: finance/asset management)

- What to do: Incorporate Kalshi-derived signals into HAR-style weekly vol forecasts and adjust position sizes inversely to predicted volatility (e.g., Moreira–Muir scaling).

- Tools/products/workflows: Python/R libraries to pull Kalshi API data, compute volume-weighted probability changes, and feed a “Kalshi-augmented HAR” forecaster to a portfolio rebalancing engine; risk dashboards showing signal percentiles and expected vol.

- Assumptions/dependencies: Regime dependence (Fed-dovish signal is most useful during active rate repricing); transaction costs and capacity may dilute gains; continued Kalshi liquidity and API access; out-of-sample gains are modest (2–4% MSFE) but statistically meaningful.

- Options market making and hedging around macro events (Sector: derivatives/market making)

- What to do: For ETH/SOL/ADA/LINK, shade implied vols lower for the week following large CPI repricing; for BTC, widen quotes or increase vega hedges when the Fed-dovish or recession-risk signals spike.

- Tools/products/workflows: Event-aware vol surface adjustments; automated straddle pricing rules keyed to KXCPI absolute moves and KXFED dovish shifts; PnL attribution by “PM-signal-aware” vs baseline.

- Assumptions/dependencies: Sufficient options liquidity (especially in altcoins); slippage and fees could erode edge; effect sizes vary by asset and time; model risk management required.

- Exchange and broker risk engines: dynamic margin and funding (Sector: centralized exchanges, prime brokers)

- What to do: Temporarily tighten BTC margin/funding when Fed-dovish/KXRECSSNBER signals spike; relax altcoin add-ons after large CPI repricing signals (expect lower realized vol).

- Tools/products/workflows: Plug-ins to risk engines that adjust SPAN/portfolio margin add-ons and funding-rate bands by signal percentile; pre-commit governance rules for transparency.

- Assumptions/dependencies: Regulatory approvals and fair access; customer communication; risk of false positives if signal regimes change.

- Client advisory and alerting (Sector: wealth/retail platforms, research desks)

- What to do: Push pre- and post-event alerts—e.g., “High Kalshi CPI repricing implies lower next-week volatility in ETH/SOL/ADA/LINK”; “Dovish Fed repricing suggests higher BTC volatility.”

- Tools/products/workflows: In-app notifications and model-backed research notes; calendar views overlaying signal spikes with expected asset-specific impact windows.

- Assumptions/dependencies: Must avoid prescriptive investment advice; maintain calibrations as regimes evolve; event clustering can blur timing.

- Market data products: Kalshi Macro Repricing Indices (Sector: data/analytics vendors)

- What to do: Package daily absolute/directional repricing indices by macro theme (Monetary Policy, CPI, Recession), plus “asset-channel maps” (BTC→Fed/Recession, ETH/SOL/ADA/LINK→CPI).

- Tools/products/workflows: Licensed API endpoints, embeddable widgets, and backtests; change-point and regime flags; cross-asset dashboards.

- Assumptions/dependencies: Kalshi API reliability and licensing; continued liquidity in key contracts; data timestamp alignment.

- Institutional treasury and stablecoin risk dashboards (Sector: fintech/treasury)

- What to do: Use KXRECSSNBER and KXFED signals to modulate BTC hedge ratios and VaR scenarios for balance sheets exposed to crypto.

- Tools/products/workflows: BI dashboards with signal percentiles mapped to VaR shock multipliers; automated hedge rebalancing tickets.

- Assumptions/dependencies: Governance thresholds for hedge changes; hedge market liquidity around events; backtest governance signoff.

- Academic replication and teaching modules (Sector: academia/education)

- What to do: Adopt the paper’s Kalshi-augmented HAR framework in econometrics/fintech courses and student projects; use signals as continuous macro uncertainty measures for event studies.

- Tools/products/workflows: Jupyter/R notebooks that fetch Kalshi data, construct signals, and run in-/out-of-sample tests; course case studies on regime dependence.

- Assumptions/dependencies: Continued public API access; clear usage rights for teaching and research.

- Editorial planning for financial media (Sector: media/research)

- What to do: Prioritize coverage when Kalshi repricing is unusually large; schedule follow-ups anticipating ETH/SOL/LINK volatility normalization after CPI events.

- Tools/products/workflows: Newsroom dashboards with thresholds triggering editor alerts; integration into macro event calendars.

- Assumptions/dependencies: Signal stability; audience value aligns with predictive content.

- ETF/SMAs overlay hedging (Sector: asset management)

- What to do: For crypto-linked ETFs or SMAs, deploy short-dated options/futures overlays keyed to Kalshi signals (e.g., add vega to BTC during Fed-dovish spikes; reduce altcoin vega post-CPI).

- Tools/products/workflows: Overlay mandates with rulebooks; signal-driven ticket generation and trade cost monitoring.

- Assumptions/dependencies: Liquidity and borrow availability; compliance review; live performance tracking.

Long-Term Applications

These ideas need further research, scaling, or productization—e.g., broader samples across multiple cycles, deeper liquidity, or regulatory development.

- Regime-aware volatility models at scale (Sector: finance/quant research)

- What to build: State-switching HAR/ML models that condition on monetary policy regimes to stabilize out-of-sample performance, especially for the BTC–Fed channel.

- Tools/products/workflows: Hidden Markov models or Bayesian regime filters; adaptive training windows; automated model choice by CSSED trends.

- Assumptions/dependencies: Longer samples spanning multiple tightening/easing cycles; model governance for dynamic switching.

- Regulatory/systemic risk dashboards (Sector: public policy/regulators)

- What to build: FSOC/CFTC/SEC dashboards integrating Kalshi macro repricing with crypto vol to monitor stress buildup and macro-crypto transmission.

- Tools/products/workflows: Multi-source feeds (Kalshi, Treasuries, implied vols) with early warning indicators; drill-down on channel-specific exposure.

- Assumptions/dependencies: Data-sharing frameworks; safeguards against spurious short-sample correlations; public–private collaboration.

- Standardized “Prediction Market Macro Factors” across asset classes (Sector: finance/benchmarks)

- What to build: Investable or reference indices of macro repricing (MonPol, CPI, Recession) used as orthogonal risk factors for equities, FX, rates, and crypto.

- Tools/products/workflows: Index governance, licensing to risk systems, analytics for factor loadings and attribution.

- Assumptions/dependencies: Sustained liquidity and low manipulation risk; cross-platform validation (Kalshi, Polymarket, etc.).

- New funds and structured products: macro-aware vol-control (Sector: asset management/structured products)

- What to build: ETFs/SMAs/notes that adjust leverage/vol targets using prediction market signals (e.g., altcoin funds that reduce vega post-CPI; BTC funds that de-risk on dovish spikes).

- Tools/products/workflows: Prospectus disclosures; real-time signal ingestion; automated overlays.

- Assumptions/dependencies: Regulatory approvals; investor demand; live track records to validate value-add.

- Clearing and exchange margining tied to prediction markets (Sector: exchanges/clearing)

- What to build: Fully automated, audited integration of PM signals into SPAN/portfolio margin for crypto derivatives, with ex-ante rulebooks and fairness constraints.

- Tools/products/workflows: Risk committee policy; kill-switches for anomalous signal behavior; continuous monitoring.

- Assumptions/dependencies: Robustness to noisy signals; prevention of procyclical feedback; regulator buy-in.

- Options surface models with PM event inputs (Sector: derivatives modelling)

- What to build: Stochastic vol/vol-of-vol models whose short-term parameters shift with PM repricing around scheduled macro events.

- Tools/products/workflows: Event calendars with calibrated impact functions; MLOps for real-time recalibration; backtesting infrastructure.

- Assumptions/dependencies: Larger datasets for calibration; demonstrable PnL stability vs baselines.

- Cross-platform prediction market composites (Sector: data/software)

- What to build: Composite macro repricing indices blending Kalshi with other venues to reduce venue-specific risk and increase coverage (e.g., non-U.S. inflation).

- Tools/products/workflows: Data normalization across contracts/thresholds; volume-based weighting; confidence scores.

- Assumptions/dependencies: Legal access to alternative venue data; harmonized contract taxonomies; manipulation detection.

- DeFi autonomous risk managers using PM signals (Sector: DeFi/protocol risk)

- What to build: On-chain oracles that feed PM repricing into dynamic collateral factors or liquidation buffers (e.g., lower LTVs for BTC when Fed-dovish rises; relax LTVs for altcoins post-CPI).

- Tools/products/workflows: Governance-approved parameter bands; oracle security; simulations of liquidation cascades.

- Assumptions/dependencies: Oracle robustness and manipulation resistance; community governance acceptance; backtests over multiple regimes.

- Corporate treasury hedging policies for crypto-exposed firms (Sector: corporates/treasury)

- What to build: Policy playbooks that trigger hedges or adjust hedging tenor based on thresholds in recession or monetary-policy repricing signals.

- Tools/products/workflows: Board-approved risk limits; automated hedge ticketing; KPI reporting.

- Assumptions/dependencies: Access to derivatives markets; hedging accounting; evidence of persistent benefit.

- Education and certification programs (Sector: education)

- What to build: Specialized certificates in prediction-market-informed risk forecasting for quants, risk managers, and traders.

- Tools/products/workflows: Curriculum based on PM signal construction, regime detection, and forecasting evaluation (CW tests, BH FDR).

- Assumptions/dependencies: Industry recognition; evolving best practices as more data accumulate.

- Policy development for broader event markets (Sector: public policy)

- What to build: Use-cases and empirical evidence to inform CFTC/SEC frameworks that enable broader macro event markets, recognizing their informational value for risk management.

- Tools/products/workflows: Pilot programs; position-limit studies; market integrity safeguards.

- Assumptions/dependencies: Stakeholder consensus; clear separation of hedging vs speculative activity.

- Retail “Macro Event Mode” in trading apps (Sector: retail fintech)

- What to build: A mode that automatically tightens risk controls (e.g., smaller default position sizes) around BTC during dovish Fed repricing and relaxes altcoin risk bands post-CPI spikes.

- Tools/products/workflows: UX controls; opt-in settings; education prompts explaining signals.

- Assumptions/dependencies: Behavioral acceptance; clear disclosures; safeguards against overfitting.

Notes on feasibility and limitations across applications:

- Channel specificity matters: BTC loads on monetary policy and recession risk; ETH/SOL/ADA/LINK load on CPI. Avalanche showed weaker results.

- Regime dependence is real: Monetary policy effects strengthened during the 2024–2025 rate-cutting cycle; recession and CPI channels were more stable out of sample.

- Signals are largely orthogonal to Fed Funds futures, Treasury returns, VIX, and crypto implied volatility (DVOL), but multiple-testing controls mean only a subset are robust at strict FDR thresholds.

- All applications rely on continued liquidity and integrity of prediction markets, accurate timestamp alignment, and awareness that effect sizes are modest but meaningful for risk management rather than pure alpha.

Glossary

- Altcoin: Any cryptocurrency other than Bitcoin, often with different risk profiles and investor bases. "The inflation channel, measured by CPI repricing on KXCPI contracts, predicts altcoin volatility for Ethereum, Solana, Cardano, and Chainlink"

- Benjamini–Hochberg correction: A multiple-testing procedure that controls the false discovery rate when running many statistical tests. "Both the Bitcoin--Fed-dovish and Chainlink--CPI specifications survive Benjamini--Hochberg correction at ."

- Binary option: A financial contract that pays a fixed amount if a specified event occurs and zero otherwise. "Each contract is a binary option on a macro outcome with a payoff of \$1 if the outcome occurs and \$0 otherwise."

- Central limit order book: A trading mechanism where all orders are matched in a single order book, typically sorted by price and time. "Contracts trade on a central limit order book with a minimum tick of \$0.01."

- Clark–West statistic: A test for whether an augmented (nested) forecasting model has better predictive accuracy than a simpler benchmark. "The Clark--West -value tests the one-sided null that the Kalshi signal adds nothing."

- CFTC-regulated event contract exchange: A marketplace for trading event-based derivatives overseen by the U.S. Commodity Futures Trading Commission. "Kalshi is the first CFTC-regulated event contract exchange in the United States"

- Consumer Price Index (CPI) repricing: Market revaluation of the probabilities attached to inflation outcomes as measured by CPI contracts. "The inflation channel, measured by CPI repricing on KXCPI contracts, predicts altcoin volatility"

- CSSED (cumulative sum of squared forecast error differences): A running total of the improvement in squared forecast errors from a new model over a baseline. "The CSSED curves show that forecast gains accumulate during the 2024--2025 rate-cutting cycle and reverse once the cycle ends."

- Deribit Bitcoin Volatility Index (DVOL): An options-implied volatility measure for crypto derived from options markets (e.g., Deribit). "We also test against the Deribit Bitcoin Volatility Index (DVOL), a crypto-specific implied volatility measure derived from BTC and ETH options."

- Directional Fed-dovish signal: A signed measure indicating downward shifts in market expectations for policy rates (dovish = lower rates). "For monetary policy, we construct a directional Fed-dovish signal: , positive when rate expectations shift downward."

- DXY index: The U.S. Dollar Index tracking the dollar’s value against a basket of foreign currencies. "All regressions include the CBOE VIX closing level, the DXY index daily return, and the S{paper_content}P 500 daily return as controls."

- EMA (exponential moving average): A weighted moving average that applies exponentially decreasing weights to older observations. "We also evaluate alternatives: a five-day exponential moving average of the lagged signal"

- Expanding-window scheme: A forecasting evaluation method where the training sample grows over time as new observations are added. "We use an expanding-window scheme with an initial training window of 120 days."

- Fed Funds futures (implied rate change): Derivatives whose prices imply market expectations for future Federal Funds rates; daily changes proxy policy repricing. "The daily change in implied Fed Funds futures rate enters as a conventional policy benchmark in orthogonalization and baseline comparison exercises."

- GARCH(1,1): A time-series model for conditional variance where current volatility depends on last period’s variance and shock. "GARCH(1,1) conditional variance: the Fed-dovish coefficient yields () for BTC"

- HAC standard errors: Heteroskedasticity and autocorrelation consistent errors that correct inference when residuals are correlated or have non-constant variance. "We use Newey--West HAC standard errors with 5 lags throughout"

- HAR (Heterogeneous Autoregressive) model: A realized volatility model capturing persistence across daily, weekly, and monthly horizons. "The Heterogeneous Autoregressive (HAR) model of \citet{corsi2009simple} is the standard benchmark for realized volatility forecasting"

- HC3 standard errors: A heteroskedasticity-robust variance estimator particularly reliable in small samples. "For non-overlapping specifications, HC3 standard errors apply."

- Implied volatility surface: A mapping of implied volatilities across strike prices and maturities inferred from options prices. "indicating that Kalshi captures macro-driven information not reflected in the options-implied volatility surface."

- Kalshi macro prediction markets: Regulated markets on Kalshi where prices reflect probabilities of macroeconomic events. "Daily probability changes in Kalshi macro prediction markets forecast cryptocurrency realized volatility through two distinct channels."

- Lead–lag test: A diagnostic comparing predictive content of lagged versus future (lead) values to check directionality of effects. "We compare a model using the lagged Fed-dovish signal () against a placebo model using the lead ()."

- Mean Squared Forecast Error (MSFE) ratio: The ratio of MSFE from an augmented model to a baseline, with values below 1 indicating improvement. "delivering an MSFE ratio of 0.979 with Clark--West ."

- Nested model comparison: An evaluation where a complex model adds variables to a simpler benchmark, enabling specific tests like Clark–West. "Table~\ref{tab:insample_btc} reports nested model comparisons for Bitcoin."

- Newey–West estimator: A method for calculating robust standard errors under heteroskedasticity and autocorrelation. "HAC standard errors (Newey--West, 5 lags) in parentheses."

- Non-farm payrolls (NFP): A key U.S. labor market statistic measuring the number of paid workers excluding certain sectors. "KXUSNFP (non-farm payrolls) has zero, reflecting the irregular listing and expiration of event-specific contracts."

- Open interest: The total value or number of outstanding derivative contracts not yet settled. "Open interest is larger and more persistent: \$278,805 at the median for KXFED, \$147,879 for KXCPI, and \$456,648 for KXRECSSNBER"

- Orthogonalization: Removing variation explained by other variables to isolate the unique information content of a signal. "The orthogonalization exercises and baseline comparisons in Section~\ref{sec:robustness} address this directly"

- Out-of-sample R2: A measure of predictive performance relative to a benchmark in data not used for model estimation. "We also report the MSFE ratio and OOS relative to the expanding historical mean."

- Overlapping observations (MA(h−1) serial correlation): Dependence induced when multi-day targets share days, creating moving-average error structure. "Five-day realized volatility creates overlapping observations with MA() serial correlation."

- Physical vs risk-neutral probabilities: Physical are real-world probabilities; risk-neutral reflect probabilities under pricing measures incorporating risk premia. "Contract prices represent risk-neutral probabilities of macro outcomes, which may diverge from physical probabilities due to risk premia"

- Prediction market: A market where securities pay based on event outcomes, aggregating dispersed information into prices. "The prediction market literature has long argued that such markets aggregate dispersed information efficiently"

- Realized volatility: A volatility measure computed from observed returns over a period, often annualized. "The dependent variable is five-day forward realized volatility:"

- Regime dependence: When a relationship holds strongly in certain economic periods but weakens or reverses in others. "but exhibits regime dependence tied to the 2024--2025 rate-cutting cycle."

- Risk-off dynamics: Market conditions where investors reduce exposure to risky assets, often raising correlations and volatility. "These absorb common risk-off dynamics that could cause Kalshi signals to serve as a metric for broad market stress."

- Risk premia: Extra expected returns required by investors to bear risk, which can separate risk-neutral from physical probabilities. "which may diverge from physical probabilities due to risk premia"

- Round-trip spread: The total cost of buying and then selling (or vice versa) due to bid–ask spreads and fees. "the implied round-trip spread is roughly two cents, widening to five cents at the tails."

- Straddle: An options strategy involving buying or selling both a call and a put at the same strike to bet on volatility. "they will systematically overprice straddles in the week following large CPI events."

- Tick size: The minimum price increment for quotes and trades. "Contracts trade on a central limit order book with a minimum tick of \$0.01."

- Treasury return (10-year Treasury): The daily return (or yield change proxy) on U.S. 10-year government bonds, often reflecting macro expectations. "we project the KXCPI signal onto the 10-year Treasury daily return"

- VIX (CBOE Volatility Index): A widely used index of expected U.S. equity market volatility derived from S&P 500 options. "All regressions include the CBOE VIX closing level"

- Volatility-managed portfolios: Strategies that scale exposure inversely with predicted volatility to stabilize risk and improve performance. "Volatility-Managed Portfolios"

- Volume-weighted averaging: Aggregating multiple instruments’ changes using traded volume as weights. "We aggregate them using volume-weighted averaging:"

- Volume-weighted probability change: A signal measuring the change in event probabilities across contracts weighted by trading volume. "The primary signal is the absolute volume-weighted change."

Collections

Sign up for free to add this paper to one or more collections.